Obesity, diabesity, food deserts and food swamps co-exist across America, factors that cost the U.S. economy over $327 billion a year just in the costs of diagnosed diabetes. In addition, America’s overweight and obesity epidemic results in lost worker productivity, mental health and sleep challenges, and lower quality of life for millions of Americans.

Food — healthy, accessible, fairly-priced — is a key social determinant of individual health, wellness, and a public’s ability to pursue happiness.

There’s a lot the U.S. can learn from the food culture, policy and economy of Italy when it comes to health.

This week, I have the honor of being a part of a contingent of Italian friends in Philadelphia welcoming two esteemed members of Italy’s medical community to my hometown: Dr. Walter Ricciardi, who leads the Istituto Superiore di Sanità (Italy’s National Institute of Health); and, Dr. Cesar Faldini, president of the Istituto Ortopedico Rizzoli in Bologna, a top hospital, academic and research center for orthopedics and trauma.

Anticipating this meeting, I wrote this appreciation about what I believe American healthcare can learn from Italy in terms of how Italians make health via a key social determinant that bolsters public and individual wellness and resilience: good food, and especially Slow Food.

Anticipating this meeting, I wrote this appreciation about what I believe American healthcare can learn from Italy in terms of how Italians make health via a key social determinant that bolsters public and individual wellness and resilience: good food, and especially Slow Food.

First, some health-economic context: note Italy’s health system performance compared with other OECD countries, pictured in the first image. Italy scores above-the-OECD-average for life expectancy, fewer deaths from heart disease, healthy weight (measured by obesity rate), and universal health insurance coverage via a national health service. [Health insurance coverage is also an important social determinant of health, but for this post, I’ll forgo that discussion — albeit a key pillar of a healthy community].

Now look out image #2: the proportion of GDP spent on healthcare by OECD nation. In 2016, the U.S. ranked as the biggest spender, allocating 17.8% of national spending on healthcare. Italy spent 8.9% of its GDP on healthcare.

The simple math is that Italy devoted 50% less as a proportion of its national economy on healthcare as America did.

Yet Italians lived longer, healthier lives than Americans. In fact, life expectancy in Italy was the second highest among all the EU countries right after Spain, the OECD noted in this report on the state of health in the European Union.

Of the many social determinants of health that make a healthy citizenry, food systems play a primary role in Italians’ health and quality of life…and especially, Slow Food.

Of the many social determinants of health that make a healthy citizenry, food systems play a primary role in Italians’ health and quality of life…and especially, Slow Food.

The third image depicts an illustration drawn during the Florentine Renaissance for De medicina, a text of Cornelius Celsus who lived between 14 BC and AD 37 and as a broad-thinking Renaissance Man, researched agriculture, medicine, and philosophy among his many intellectual interests. Celsus composed De medicina largely based on the teachings of Hippocrates.

Book I of the eight volumes Celsus wrote covered diet, hygiene, and the benefits of exercise.

Fast-forward two thousand years, and we’re still preaching the benefits of nutrition and physical activity. The Slow Food movement grew out of this understanding, beginning in Italy in 1986 in response to a McDonald’s franchise opening in Rome.

Carlo Petrini, a journalist, organized a group of people to greet passersby near the Spanish Steps where the fast-food restaurant was planning to open, passing out bowls of penne pasta.

“We don’t want fast food,” they said. “We want slow food.”

Thus the Slow Food organization was born, inspiring branches around the world, from towns from “A” to “Z” — from Adelaide, Australia, to Zagreb, Croatia. In fact, there are over 1,500 Slow Food “convivia,” or chapters, around the world.

Back to Italy, the birthplace of Slow Food, then inspired another “slow” phenomenon that can profoundly impact good health: Slow Medicine.

The first mention of Slow Medicine was in an Italian medical journal on cardiology, published sixteen years after the birth of Slow Food.

Dr. Alberto Dolara, an Italian cardiologist, wrote in the Italian Heart Journal (translated into English), “In clinical practice, hyperactivity is often unnecessary. Adopting a strategy of ‘slow medicine’ may be more rewarding in many situations. Such an approach would allow health professionals and in particular doctors and nurses, to have sufficient time to evaluate the personal, familial and social problems of the patient extensively, to reduce anxiety whilst waiting for non-urgent diagnostic and therapeutic procedures, to evaluate new methods and technologies carefully, to prevent premature dismissals from hospital and finally to offer an adequate emotional support to the terminal patient and their families.”

Dr. Alberto Dolara, an Italian cardiologist, wrote in the Italian Heart Journal (translated into English), “In clinical practice, hyperactivity is often unnecessary. Adopting a strategy of ‘slow medicine’ may be more rewarding in many situations. Such an approach would allow health professionals and in particular doctors and nurses, to have sufficient time to evaluate the personal, familial and social problems of the patient extensively, to reduce anxiety whilst waiting for non-urgent diagnostic and therapeutic procedures, to evaluate new methods and technologies carefully, to prevent premature dismissals from hospital and finally to offer an adequate emotional support to the terminal patient and their families.”

Note the three Italian words below the snails in the Slow Medicine image: “Sobria, Rispettosa, Giusta.” In English, these are,

– Measured

– Respectful, and

– Equitable.

Imagine if…in the U.S. doctor-patient relationship, we adopted “measured” medicine, in not over-treating or wasting resources, but using the right therapy and technology in the right patient at the right time? What if we baked respect into our system, between physicians and patients, between professionals at-work, where individuals’ values and desires were given voice? What if the U.S. health system embraced equity, first being honest about our health disparities and implementing policies and practices to eliminate those disparities, realizing quality, affordable care for all?

Health Populi’s Hot Points: In full transparency, while I hold a U.S. passport as an American citizen, I am also a citizen of Italy. As such, I am a citizen of the EU. In the EU, people who live in the community are also known as “health citizens.”

Health Populi’s Hot Points: In full transparency, while I hold a U.S. passport as an American citizen, I am also a citizen of Italy. As such, I am a citizen of the EU. In the EU, people who live in the community are also known as “health citizens.”

We are not really health citizens in America. We don’t have what Dr. Ricciardi recently spoke about in this video — “la salute e uguale per tutti” — health and equality for all.

Dr. Ricciardi’s remarks were part of this campaign, shown here. Translated into English, the two sentences say:

Health is the same for everyone, and a right to be spread through Italy.

Do it with a kiss, like a virus that is good for our country and an appeal that cannot be stopped.

Would that we in America could embrace such a public health message for all.

The post Slow Food, Slow Medicine: What Italy Can Teach America About Health appeared first on HealthPopuli.com.

Slow Food, Slow Medicine: What Italy Can Teach America About Health posted first on http://dentistfortworth.blogspot.com

Health Populi’s Hot Points: Trust is a precursor to health engagement, and especially underpins one’s willingness to share personal health data. Trust works in the other direction, too — as sources of medical information. The second image shows that health consumers most-trust academic medical centers (teaching hospitals) and professional medical associations, along with community hospitals and pharmacies, as sources of reliable information on treatments.

Health Populi’s Hot Points: Trust is a precursor to health engagement, and especially underpins one’s willingness to share personal health data. Trust works in the other direction, too — as sources of medical information. The second image shows that health consumers most-trust academic medical centers (teaching hospitals) and professional medical associations, along with community hospitals and pharmacies, as sources of reliable information on treatments. Most physicians feel some level of burnout, hassled by electronic health records and lost autonomy. No wonder, then, that a majority of doctors favor some type single payer health system — one-quarter fully single payer, a la Britain’s National Health Service; and another one-third a single payer combined with a private insurance option, discovered in the

Most physicians feel some level of burnout, hassled by electronic health records and lost autonomy. No wonder, then, that a majority of doctors favor some type single payer health system — one-quarter fully single payer, a la Britain’s National Health Service; and another one-third a single payer combined with a private insurance option, discovered in the

Health Populi’s Hot Points: We now call upon our physicians to also be health economists, evaluating patients’ social determinants of health — personal factors related to poverty or other social conditions. About 9 in 10 doctors say at least some of their patients have a serious health problem that’s linked to a social determinant.

Health Populi’s Hot Points: We now call upon our physicians to also be health economists, evaluating patients’ social determinants of health — personal factors related to poverty or other social conditions. About 9 in 10 doctors say at least some of their patients have a serious health problem that’s linked to a social determinant.

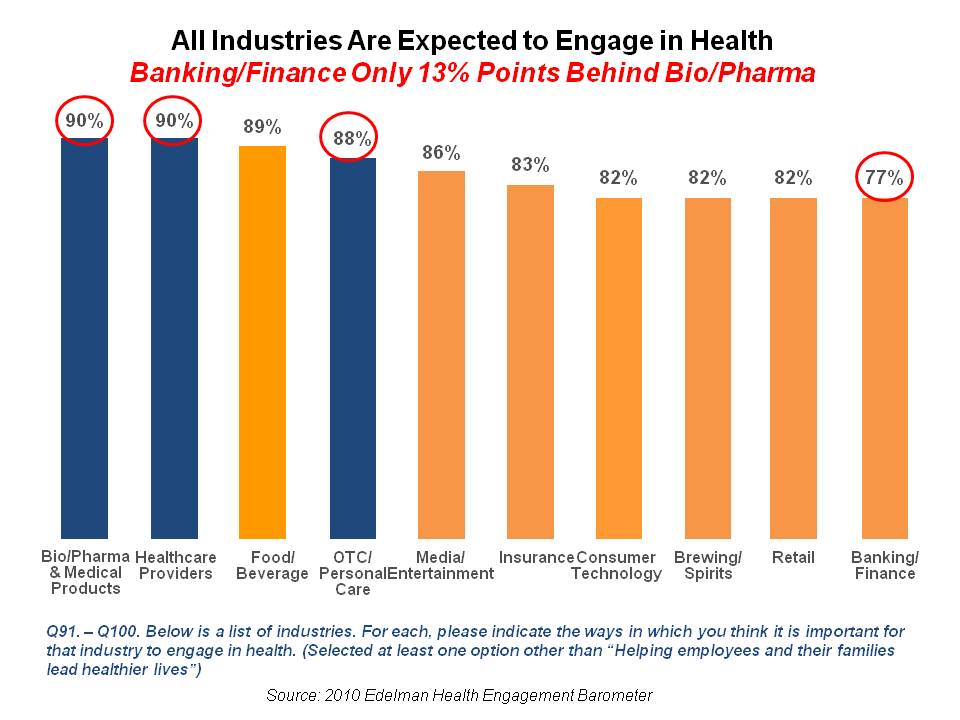

Most consumers look to every industry sector to help them engage with their health.

Most consumers look to every industry sector to help them engage with their health.

Health Populi’s Hot Points: The health/care ecosystem continues to morph, with data-tracking-and-sharing, along with behavioral economics, baked into consumer-facing healthcare products and services. This is all about behavior change, and nudging (perhaps forcing) consumers to take on more responsibility: for financial and clinical decisions. Privacy, too, is a question in this and other data-sharing programs. Not only do wearable tech devices “leak” data that many consumers assume to be kept secure, but what about the opt-in for the insurance programs? What if a consumer wants to share certain data, but not other personally-generated information from, say, the bedroom or bathroom?

Health Populi’s Hot Points: The health/care ecosystem continues to morph, with data-tracking-and-sharing, along with behavioral economics, baked into consumer-facing healthcare products and services. This is all about behavior change, and nudging (perhaps forcing) consumers to take on more responsibility: for financial and clinical decisions. Privacy, too, is a question in this and other data-sharing programs. Not only do wearable tech devices “leak” data that many consumers assume to be kept secure, but what about the opt-in for the insurance programs? What if a consumer wants to share certain data, but not other personally-generated information from, say, the bedroom or bathroom? Just don’t get Twine Health confused with Twine, a financial wellness subsidiary of John Hancock.

Just don’t get Twine Health confused with Twine, a financial wellness subsidiary of John Hancock.

Remember that President Trump promised American voters in his TIME magazine Person of the Year interview in December 2016 that he would drive down Rx costs for consumers — because, as he has often said,

Remember that President Trump promised American voters in his TIME magazine Person of the Year interview in December 2016 that he would drive down Rx costs for consumers — because, as he has often said,

Health Populi’s Hot Points: Americans are stressed by out-of-pocket healthcare costs, the second chart shows, so there’s a double-whammy health effect here: first, financial, where people who could optimize healthcare spending by saving in an FSA or HSA. Second, a mental and potentially physical health impact from that financial stress.

Health Populi’s Hot Points: Americans are stressed by out-of-pocket healthcare costs, the second chart shows, so there’s a double-whammy health effect here: first, financial, where people who could optimize healthcare spending by saving in an FSA or HSA. Second, a mental and potentially physical health impact from that financial stress.

Nudging people to save more overall – specifically for healthcare — will need a lot more than a clever digital tool and “knowledge.” We’ve known about the compelling triple-tax advantage of a health savings account since President Bush promoted them in 2006. Twelve years later, what looks fiscally compelling on paper just hasn’t inspired people to save more for much of anything — let alone healthcare expenses.

Nudging people to save more overall – specifically for healthcare — will need a lot more than a clever digital tool and “knowledge.” We’ve known about the compelling triple-tax advantage of a health savings account since President Bush promoted them in 2006. Twelve years later, what looks fiscally compelling on paper just hasn’t inspired people to save more for much of anything — let alone healthcare expenses. Underneath that “how” is more than the next-best-me-too-product for allergy or acne. It’s about efficacy of the product at the core, but bundled with social responsibility and sustainability, informative packaging, transparency of ingredients, and education that empowers the individual.

Underneath that “how” is more than the next-best-me-too-product for allergy or acne. It’s about efficacy of the product at the core, but bundled with social responsibility and sustainability, informative packaging, transparency of ingredients, and education that empowers the individual. Health Populi’s Hot Points: With the health consumer always-on and connected, authenticity, evidence, and transparency are in-demand.

Health Populi’s Hot Points: With the health consumer always-on and connected, authenticity, evidence, and transparency are in-demand.

Note this messaging found on the children’s wellness brand, Jack and Jill, one of the GMDC Showcase participants: “free from all nasties.” This, in products marketed to parents for kids.

Note this messaging found on the children’s wellness brand, Jack and Jill, one of the GMDC Showcase participants: “free from all nasties.” This, in products marketed to parents for kids.{kind=link}