Googling the words “disruption” and “healthcare” today yielded 33.8 million responses, starting with “Riding the Disruption Wave in Healthcare” from Bain in Forbes, Accenture’s essay on “Big Bang Disruption in Healthcare,” and, “A Cry for Encouraging Disruption” in the New England Journal of Medicine Catalyst. This last article responded to the question, “Can we successfully deliver better quality care for patients at a lower cost?” asked by François de Brantes, Executive Director of the Health Care Incentives Improvement Institute.

Googling the words “disruption” and “healthcare” today yielded 33.8 million responses, starting with “Riding the Disruption Wave in Healthcare” from Bain in Forbes, Accenture’s essay on “Big Bang Disruption in Healthcare,” and, “A Cry for Encouraging Disruption” in the New England Journal of Medicine Catalyst. This last article responded to the question, “Can we successfully deliver better quality care for patients at a lower cost?” asked by François de Brantes, Executive Director of the Health Care Incentives Improvement Institute.

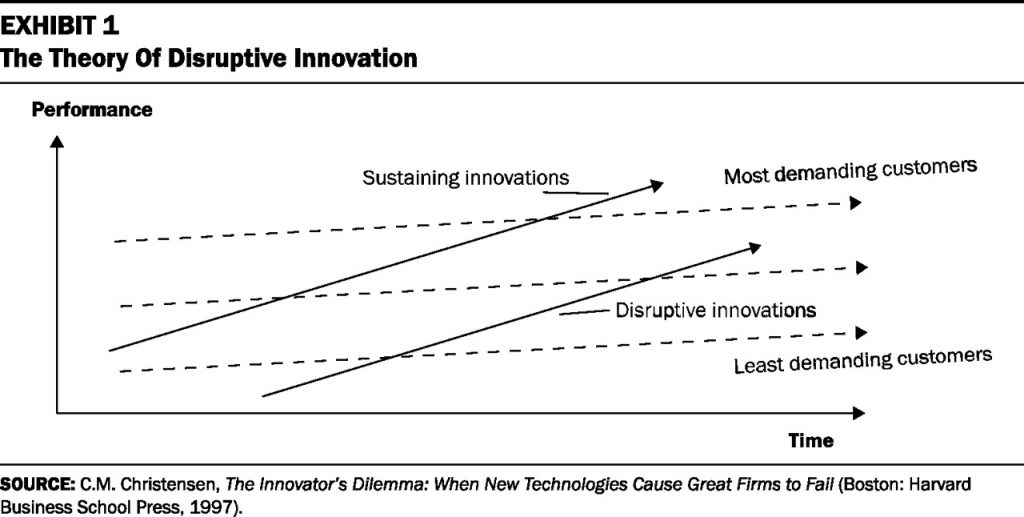

“Disruption” as a noun and an elephant in our room has been with us in healthcare since the September/October 2000 issue of Harvard Business Review. In that issue, Clay Christensen and colleagues published their seminal article, Will Disruptive Innovations Cure Healthcare? This emerged out of Christensen’s 1997 book, The Innovator’s Dilemma. Since then, U.S. health care industry wonks (including me) have used the “d” word in conversation, presentation, and prognostication.

But it took some years to get “here,” to this point in American healthcare’s moment of exorbitant spending, inefficiency, burnt-out clinicians, and universal frustration across industry stakeholders, for me to say that disruption is not a point sitting on Gartner’s Hype Cycle: disruption is now the new normal in American healthcare.

Just this week, JAMA features a Viewpoint column titled, How Disruptive Innovation by Business and Technology Firms Could Improve Population Health. And, a new survey from Reaction Data on the future of the healthcare market focuses on the theme of “healthcare disruption.”

This isn’t just a word that we’ve been waiting to “happen.” This is happening, and as the founder of Institute for the Future, Roy Amara first coined: We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.

This isn’t just a word that we’ve been waiting to “happen.” This is happening, and as the founder of Institute for the Future, Roy Amara first coined: We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.

Dr. Anne Stey and her UCSF colleagues write in JAMA, “The entrance of the business and technology sector in the health care market creates an opportunity because of the accessible platforms, analytics, and marketing expertise that many of these companies already have in place.”

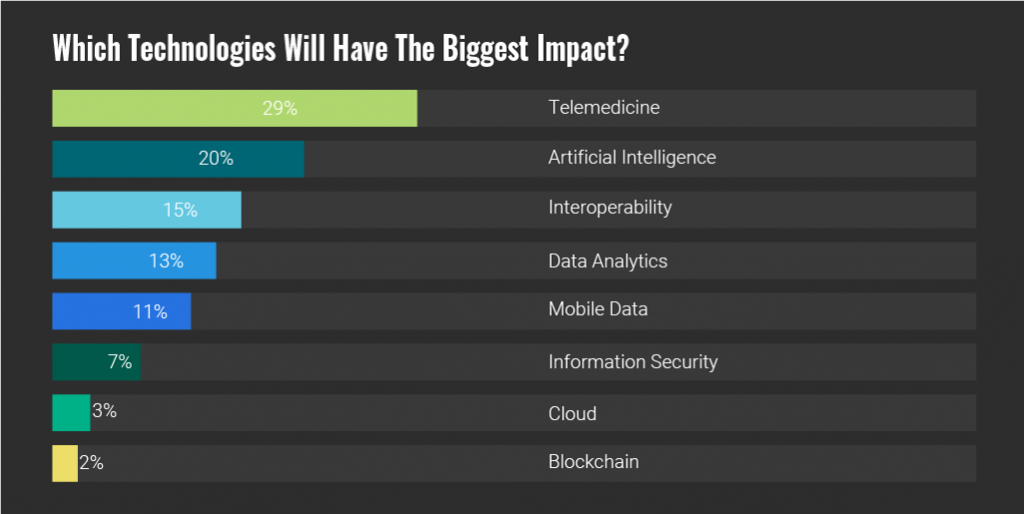

Now, turn to the Reaction Data study’s chart on which technologies will have the biggest impact. Note that respondents to this study were mostly C-level executives working in hospitals. They said that the technologies that would have the largest disruptive impact would be telemedicine, artificial intelligence, interoperability, and data analytics. These are some of the very things Dr. Stey’s article on disruption cite.

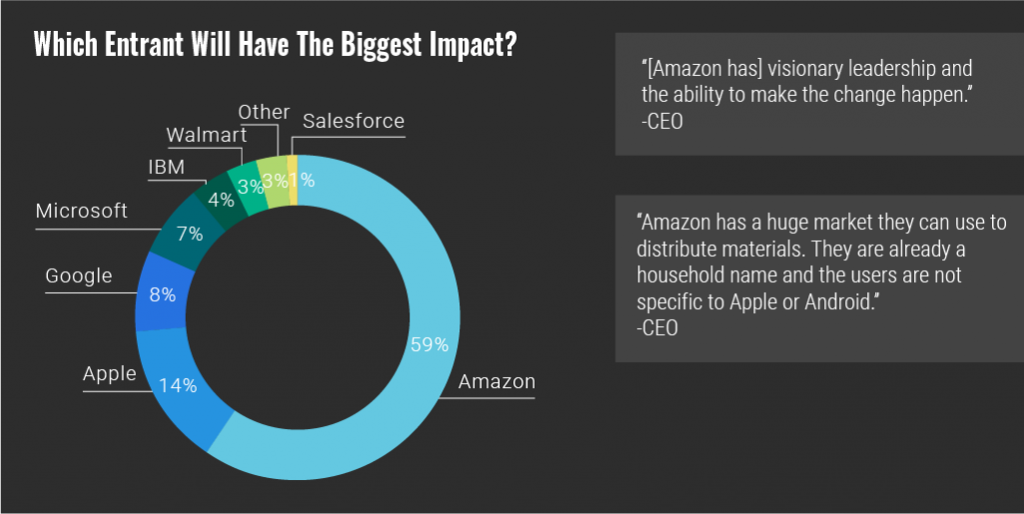

Which new entrant would likely have the greatest impact? Reaction Data asked.

That would be Amazon, Apple, Google, Microsoft, followed by IBM, Walmart and Salesforce, the second chart from Reaction Data shows you.

This finding confirms what we’ve been saying here on Health Populi for a while…my Institute for the Future mentors taught me well (thank you Ian, Wendy, Robert, Mary and Matthew. et. al.). Here’s more on Amazon, on Apple, on Google, and Microsoft, if you care to dig in to each of these more.

Health Populi’s Hot Points: So exactly 20 years after Christensen wrote The Innovator’s Dilemma, he gave a seminar on how disruptive innovation can finally revolutionize healthcare. “Finally,” after 20 years….which is why I continue to keep Amara’s Law front-of mind when it comes to healthcare’s ability to change.

Health Populi’s Hot Points: So exactly 20 years after Christensen wrote The Innovator’s Dilemma, he gave a seminar on how disruptive innovation can finally revolutionize healthcare. “Finally,” after 20 years….which is why I continue to keep Amara’s Law front-of mind when it comes to healthcare’s ability to change.

Dr. Stey’s Viewpoint recognizes that the drive real change in healthcare that impacts peoples’ health, it’s critically important to connect healthcare providers to the new-new innovations. Consumers-patients highly trust their doctors, their nurses, their pharmacists, above all professions in the U.S. Making those connections via telehealth and virtual health technology, from a pure technical standpoint, is do-able today.

The larger challenge, Stey and friends point out, is access: too many patients lack either insurance or other convenient on-ramps to primary care. Empowering individuals with access to their own health records – that is, their own data — could help make these connections, and make them stick. That’s not a panacea and won’t solve the larger access challenge, but will help.

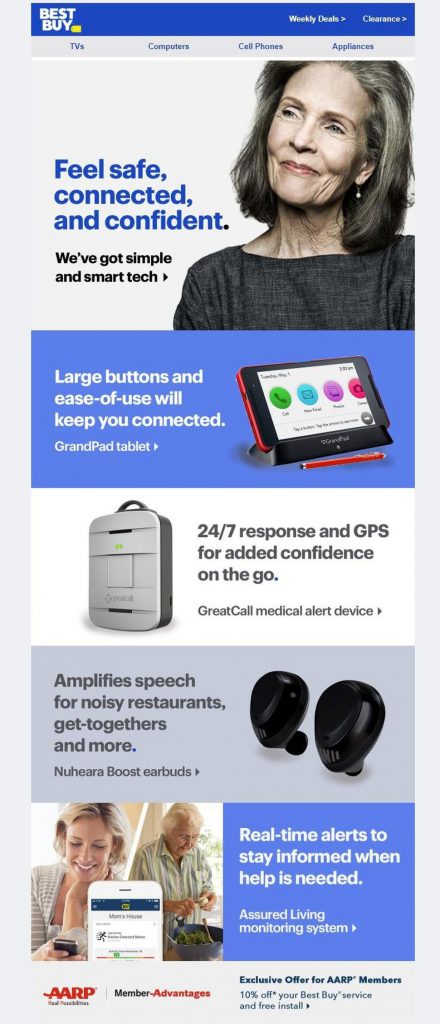

In the past few days, we see that Amazon has hired a star cardiologist to join the company’s healthcare efforts; Walmart will work with Anthem, the health insurance group, to expand access to over-the-counter medicines; Best Buy is buying GreatCall to expand retail health to older people; and Capsule, a digital pharmacy, raised $50 million more in funding to try and scale nationally….among other pretty big stories that fall into the “disruptive” category.

Not every one of these efforts will stick or scale…but they aren’t pilots or mini-experiments for fast-failure, either. We have entered the chaos-and-creation phase of healthcare disruption. Let’s buckle in, lean in, learn together, and drive that Quadruple Aim to make healthcare better, cheaper, accessible, for all. To paraphrase the wise François de Brantes of HCCI, we must deliver better quality care for all patients at a lower cost.

The post Disruption Is Healthcare’s New Normal appeared first on HealthPopuli.com.

Disruption Is Healthcare’s New Normal posted first on

http://dentistfortworth.blogspot.com

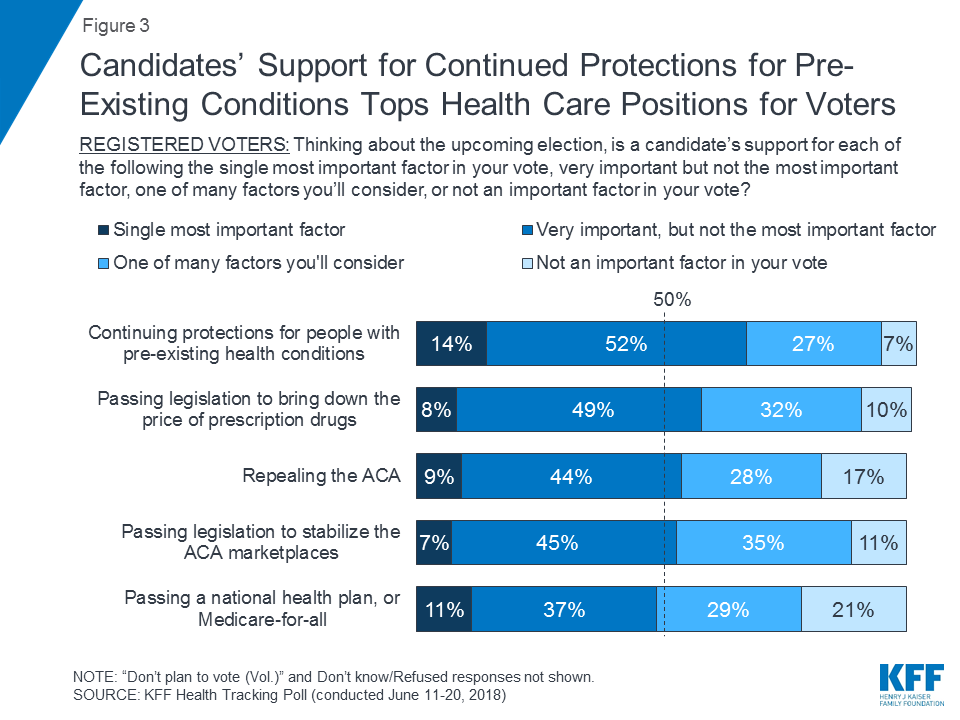

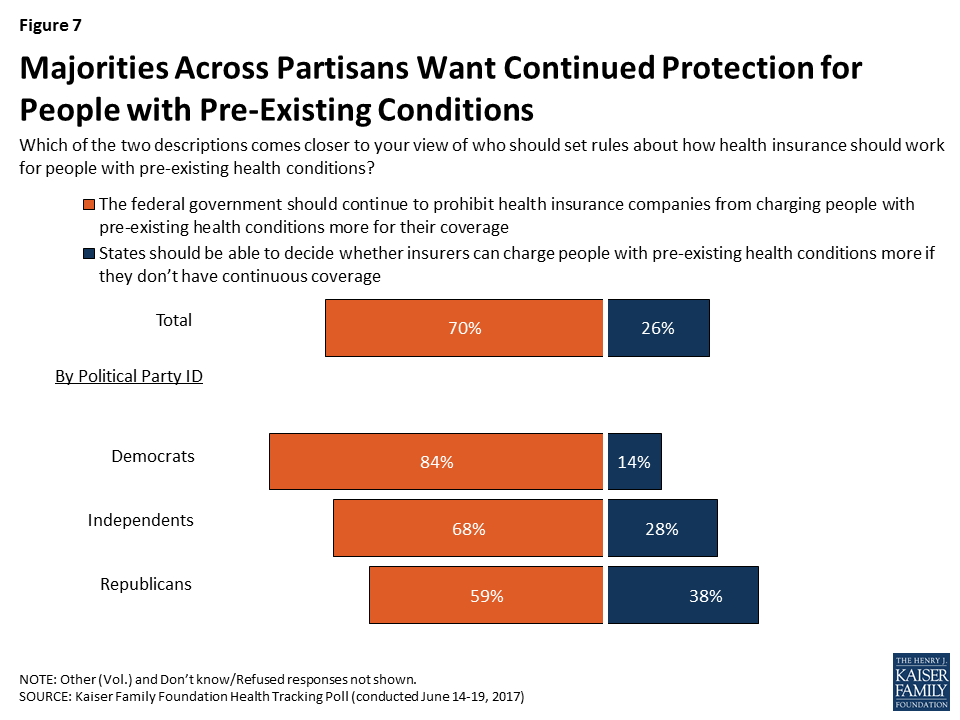

Health Populi’s Hot Points: Pre-existing conditions are a big deal to Americans these days: among registered voters, ensuring that health plans cover pre-existing conditions is the most important health care issue on Americans’ minds,

Health Populi’s Hot Points: Pre-existing conditions are a big deal to Americans these days: among registered voters, ensuring that health plans cover pre-existing conditions is the most important health care issue on Americans’ minds,

As Bruce Springsteen presciently sang in 1984 on the Born in the USA album, “Cover Me” — whichever town or state I live in, and whatever my political party ID.

As Bruce Springsteen presciently sang in 1984 on the Born in the USA album, “Cover Me” — whichever town or state I live in, and whatever my political party ID.

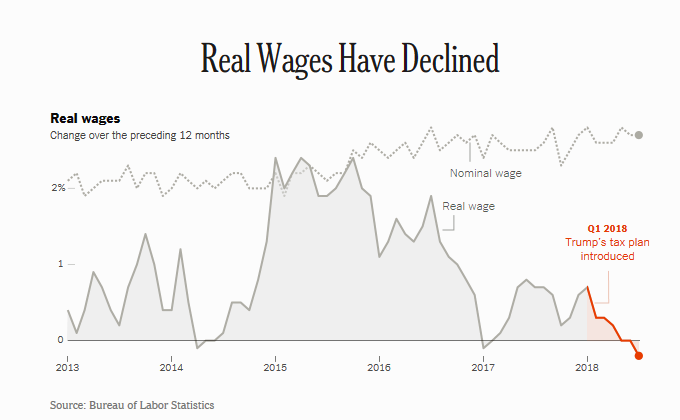

Health Populi’s Hot Points: Workers’ real wages have declined in the past year, owing to higher oil prices (translating at the gas tank) which off-set any modest increases in income Americans might have seen in their paychecks from the 2018 tax cut bill.

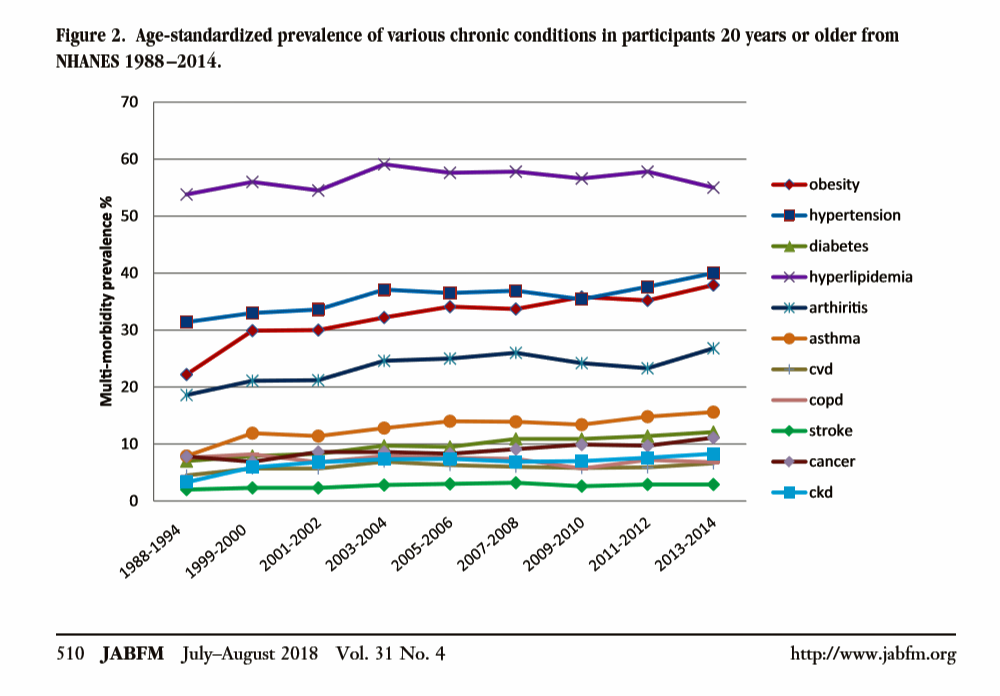

Health Populi’s Hot Points: Workers’ real wages have declined in the past year, owing to higher oil prices (translating at the gas tank) which off-set any modest increases in income Americans might have seen in their paychecks from the 2018 tax cut bill. In the U.S., the growing prevalence of multi-morbidity is contributing to increased mortality and healthcare cost growth in America. Underlying this clinical and economic phenomenon is obesity, which primary care doctors are challenged to deal with as a chronic condition along with typically co-occurring comorbidities of hypertension, diabetes, and hyperlipidemia.

In the U.S., the growing prevalence of multi-morbidity is contributing to increased mortality and healthcare cost growth in America. Underlying this clinical and economic phenomenon is obesity, which primary care doctors are challenged to deal with as a chronic condition along with typically co-occurring comorbidities of hypertension, diabetes, and hyperlipidemia. Health Populi’s Hot Points: I note that the authors of this study are based at the West Virginia University Department of Family Medicine. I’ve frequently looked at West Virginia here in Health Populi and elsewhere as a state that bears a heavy public health burden based on a range of risk factors: smoking, health care service access and insurance coverage (with 29% of the state’s citizens covered by Medicaid, the highest share of a U.S. state’s population enrolled in the plan), and, yes, obesity.

Health Populi’s Hot Points: I note that the authors of this study are based at the West Virginia University Department of Family Medicine. I’ve frequently looked at West Virginia here in Health Populi and elsewhere as a state that bears a heavy public health burden based on a range of risk factors: smoking, health care service access and insurance coverage (with 29% of the state’s citizens covered by Medicaid, the highest share of a U.S. state’s population enrolled in the plan), and, yes, obesity.

With the acquisition of GreatCall, a mature player in the aging-tech space, Best Buy is doubling down on consumer health technology@retail.

With the acquisition of GreatCall, a mature player in the aging-tech space, Best Buy is doubling down on consumer health technology@retail. “We have a great opportunity to serve the needs of these customers by combining GreatCall’s expertise with Best Buy’s unique merchandising, marketing, sales and services capabilities,” CEO Hubert Joly was quoted in the press release on the deal.

“We have a great opportunity to serve the needs of these customers by combining GreatCall’s expertise with Best Buy’s unique merchandising, marketing, sales and services capabilities,” CEO Hubert Joly was quoted in the press release on the deal. Health Populi’s Hot Points: Best Buy ranks top of the list of top 100 consumer electronics retailers as tallied by TWICE, a leading publication on the consumer electronics industry who partners with CTA (the Consumer Technology Association, operator of the annual CES conference).

Health Populi’s Hot Points: Best Buy ranks top of the list of top 100 consumer electronics retailers as tallied by TWICE, a leading publication on the consumer electronics industry who partners with CTA (the Consumer Technology Association, operator of the annual CES conference).