- FHIR.

- Measuring trust in physicians.

- Neighborhood effects on BMI.

- Dentists earn monopoly rents?

- Does having kids make you happy?

- “Sell it all.”

Friday Links posted first on http://dentistfortworth.blogspot.com

CVS + Aetna have merged to evolve a new business model for health and medical care. Walgreen’s continues to add new services beyond the core pharmacy business, and Walmart is expanding telehealth and healthier food aisles in the grocery. More grocery stores added dietitians to their operations in 2018, as well.

As people take on more self-care for health care, they are looking to access products and services in retail bricks-and-mortar and ecommerce channels in the same places they buy food and other products. ACSI’s latest customer satisfaction benchmark study into retailers provides insights into the trusted channels for retail health in 2019.

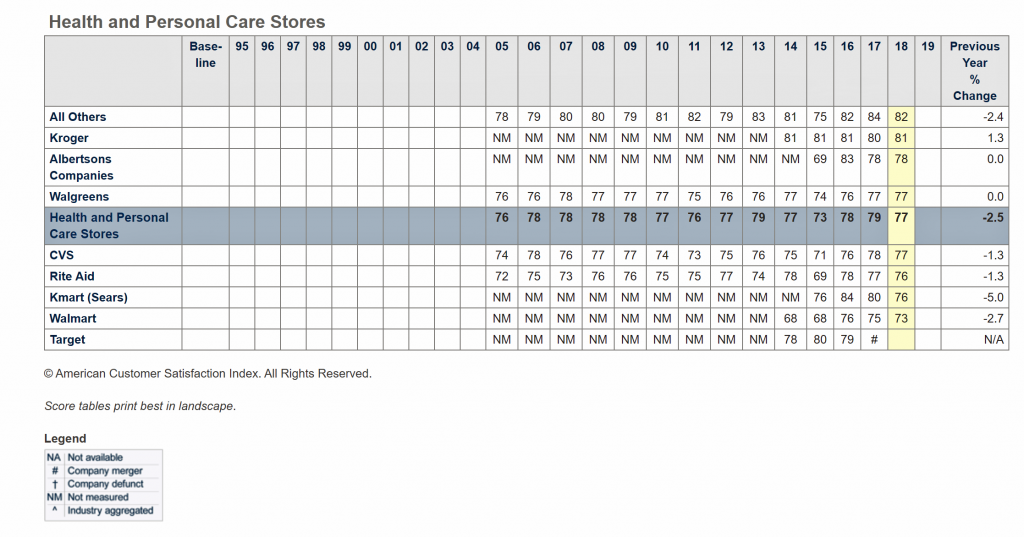

The American Customer Satisfaction Index (ACSI) annually gauges 300,000 U.S. consumers’ experiences with 400 companies in 46 industries. In the ACSI study, “health and personal care stores” are pharmacy and drug stores.

The American Customer Satisfaction Index (ACSI) annually gauges 300,000 U.S. consumers’ experiences with 400 companies in 46 industries. In the ACSI study, “health and personal care stores” are pharmacy and drug stores.

ACSI’s research found U.S. consumers’ highest-ranked health and personal care stores in 2018 were Kroger, Albertsons companies (with storefronts such as ACME, Jewel-Osco, Safeway and Vons), and Walgreens, shown by the first chart. Below the mean for health and personal care were CVS, Rite Aid, Kmart (Sears), Walmart and Target.

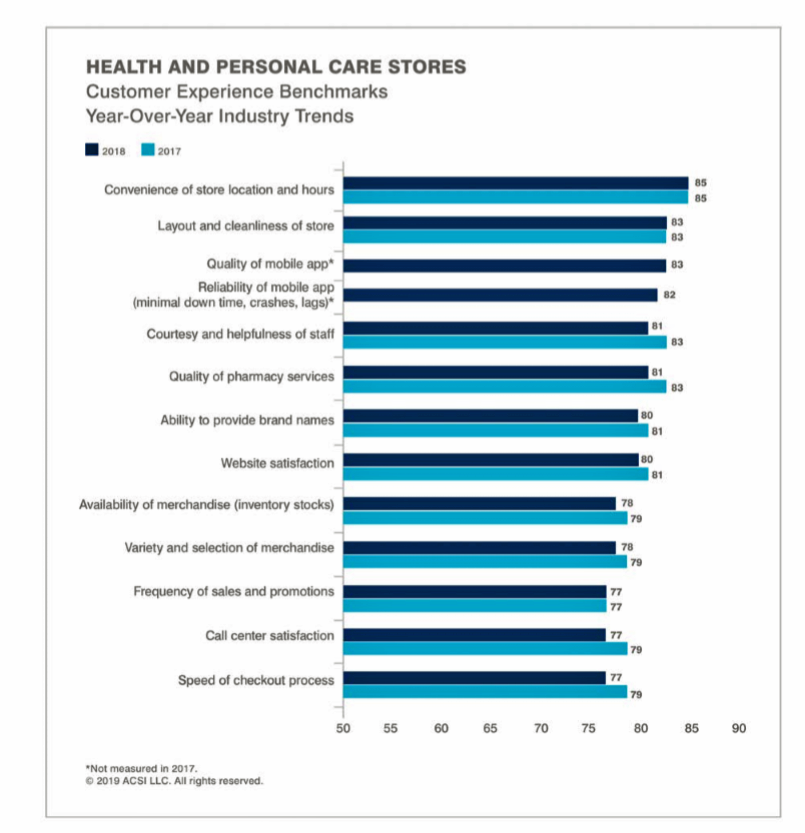

Consumers most highly value certain features when they rate their experience with health and personal care stores, including the convenience of store locations, the layout and cleanliness of stores, quality and reliability of the store’s mobile app, and quality of pharmacy services, among other metrics.

ACSI found that between 2017 and 2018, the customer experience benchmark for health and personal care stores fell by 2.5 percentage points.

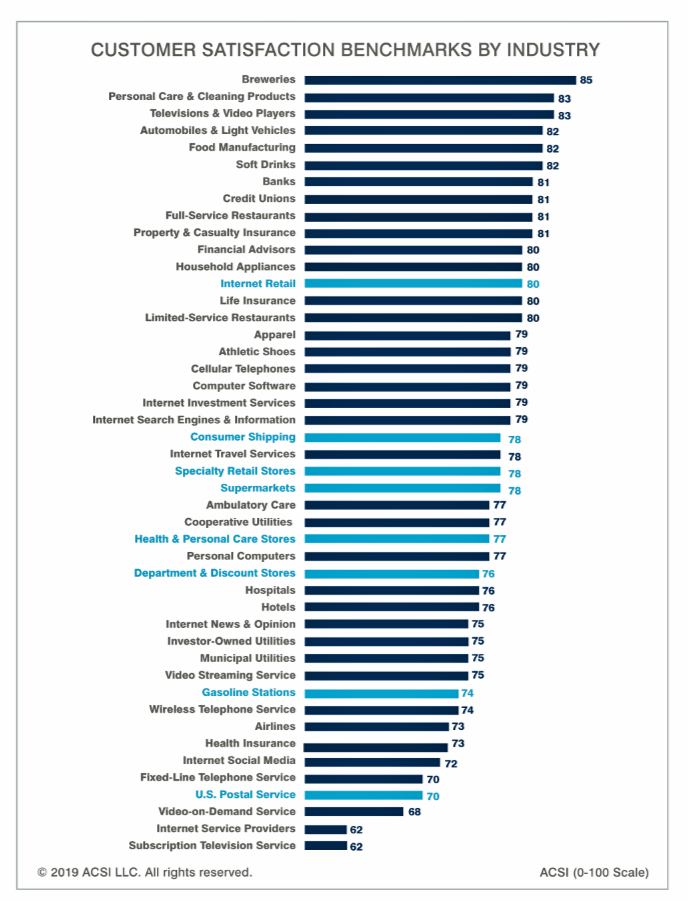

Health Populi’s Hot Points: The third graphic arrays the sectors ACSI gauges for customer satisfaction. Note that breweries, personal care and cleaning products (THINK: J&J, P&G), TVs, cars, food and beverages rank the highest among U.S. consumers.

Health Populi’s Hot Points: The third graphic arrays the sectors ACSI gauges for customer satisfaction. Note that breweries, personal care and cleaning products (THINK: J&J, P&G), TVs, cars, food and beverages rank the highest among U.S. consumers.

Health care segments — ambulatory care, hospitals, and health insurance, along with health and personal care stores (pharmacies/drug stores) rank well below consumers’ satisfaction with beers, cars, and banks.

In my read and forecasting of the growing ecosystem of retail health, I’ll share with you that my own advisory work has recently found me providing input into the business plans of…breweries, auto companies, and financial services firms.

These industries now understand that they are important touchpoints into consumers’ very personal definitions of what constitutes health and wellness: holistic living, social connections, good food and good times, and financial wellness.

The post Consumers’ Trust In Health And Personal Care Stores: The Growing Retail Health Ecosystem appeared first on HealthPopuli.com.

IVI will be hosting two webinars introducing our new open-source value model in non-small cell lung cancer. Devin Incerti and Jeroen Jansen will lead the webinar tomorrow.

Date: February 27, 2019 at 2:30 PM EST / 11:30 AM PST

Content: In-depth discussion of technical and methodological aspects of the IVI-NSCLC model

OSVP models are built to be entirely open-source, allowing anyone to customize the tool depending on their own assumptions and understanding of value. Join us for a webinar to learn more about how the IVI model generates customized information on non-small cell lung cancer treatments and how to apply the information in assessing value in health care. Please click here to register and reserve your spot!

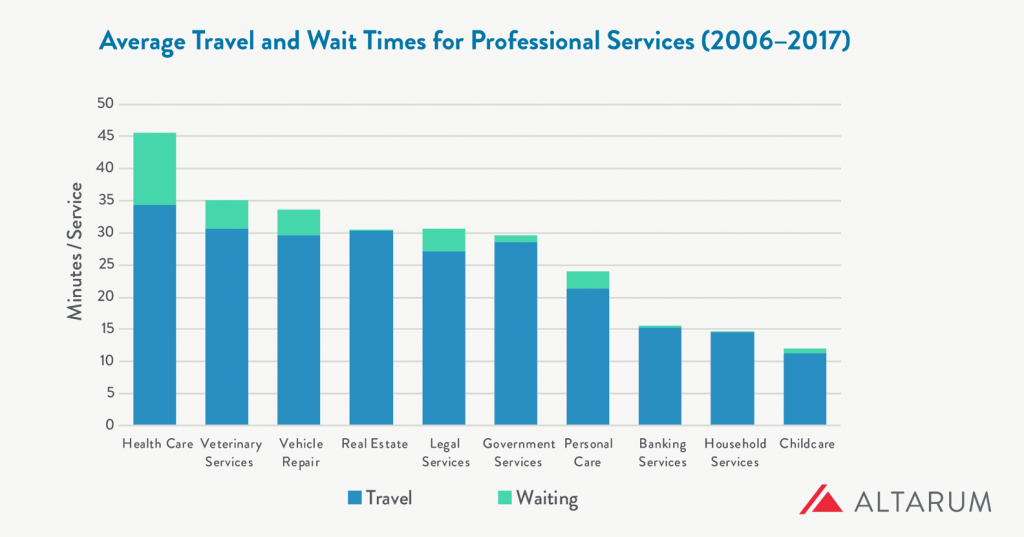

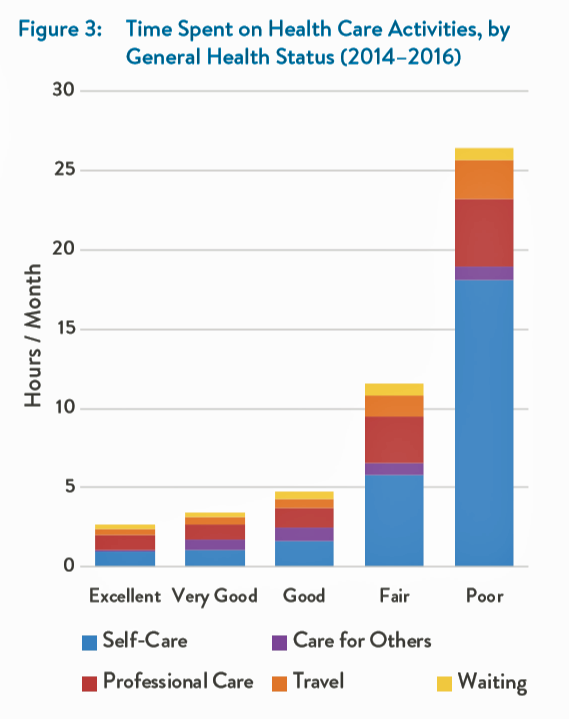

What industry compels its “consumers” to wait longer and travel further for services more than any other in a person’s daily life?

That would be health care, a report from Altarum notes.

People travel further and wait longer for medical services than for veterinary care (second in this line-up), auto repair, banking, and household services.

The annual opportunity cost for travel and wait time in health care is $89 billion, Altarum estimated.

For the average person, that translates to 34 minutes of travel time and 11 minutes waiting time at the provider’s office.

In terms of personal opportunity costs, Altarum gauged the following lost-times:

Read this last bullet point again. Then, take a look at this layered bar chart which illustrates the direct straight line relationship between the time a person spends on health care activities and that person’s health status. It’s simple to see that people in poor health spend much more time in a day on self-care than healthier people. Sicker people also spend much more time traveling to health care appointments.

The person in poor health would also more likely be unemployed or out of the labor force, which underscores the importance of the travel-time challenge.

Health Populi’s Hot Points: I snapped this photo, a promotional ad from Lyft, at HIMSS19 in Orlando two weeks ago. This was the first image that greeted me as I entered the Orange County Convention Center to retrieve my badge for the conference.

Health Populi’s Hot Points: I snapped this photo, a promotional ad from Lyft, at HIMSS19 in Orlando two weeks ago. This was the first image that greeted me as I entered the Orange County Convention Center to retrieve my badge for the conference.

“90% of seniors say access to Lyft improves their quality of life,” the company gleaned from a consumer survey they conducted and reported in Fast Company. Check out the brand associated with this message at the bottom of the poster: it’s from AARP, which is an association of 38 million people over the age of 50, a key bloc of consumers looking to age well and prosper as long as they can.

There’s travel time, and there’s quality time. Considering the “poor health” bar in the graph, we can see the opportunity for telehealth and home visits to people who may have mobility and other challenges leaving the home space. Our homes are evolving into our health hubs — truly our “medical homes,” which have been formally defined as a primary care gatekeeper’s office. Why should that be, in a physical sense?

An article published in Health Services Research in August 2018 talks about Trends in the Types of Usual Sources of Care: A Shift from People to Places or Nothing at All. The Accenture health care team shared this with me at HIMSS19 in the context of their research into consumer demands for alternate sites of medical services, from retail clinics to virtual platforms.

“The positive, salutary effects of having a USC have been documented for decades,” the authors note. “Usual Sources of Care” (USCs) have been associated with higher quality, reduced unmet needs, and fewer health disparities, previous research has found. Even for uninsured people in the U.S., having a usual point of contact for health care is an on-ramp to preventive services and physician visits.

But what if the in-person, bricks-and-mortar model shifts to more virtual, more local, more convenient channels of care? What might a USC in contemporary, digitally-enabled formats look and feel like? What if that “place” was our home, first and foremost?

That’s what some of us are working on these days. Stay tuned…

The post Time To Travel And Wait In Health Care: The Opportunity For Self-Care At Home appeared first on HealthPopuli.com.

So you want to compare two treatments–for instance Treatment A and Treatment B–in order to see which one has largest impact on health outcomes. Sure you could do a randomized controlled trial, but let’s say you don’t have the funding for that. You could use real world data to conduct just such an analysis. Let’s say you are an econometric expert and you address selection bias with fancy techniques (e.g., instrumental variables, regression discontinuity, stratified covariate balancing). Problem solved, right?

Not so fast. The approach above assumes that one set of patients take Treatment A and stay on the treatment and the other set of patients take Treatment B. In the real world, however, patients may often switch between medications or even discontinue medications. What do you do in this case?

One approach to address this issue is to implement a marginal structural model (MSM). This approach examines the differences in treatment histories to measure the marginal impact of switching from one medication to another over the course of the observed data. As described in Faries and Kadziola:

An MSM analysis is basically a weighted repeated measures approach — using treatment as a time-varying covariate. Weights, based on inverse probability of treatment weighting, control for time-dependent confounders and essentially produce a pseudo-population with balance in both time-invariant and time-varying covariates allowing for causal treatment comparisons using standard repeated measures models.

In practice, creating an MSM involves calculating two weights: one for treatment selection and the other for discontinuation. The treatment selection weight is:

SW = Πk=0 to t {f[a(k)|A(k-1),V]}/{f(a(k)|A(k-1),L(k)]}

where a(k) is treatment at time k, A(k-1) is the entire treatment history through time k-1, V is a vector of time-independent baseline covariates, and L(k) is a vector of time-varying covariates through time t. Note that L(k) also includes baseline covariates V. The numerator above is the probability of receiving a treatment at time k, conditional on treatment history and baseline characteristics; the denominator is the same factor, but it it incorporates time-varying factors .

The second set of weights accounts for patient dropout. The stablized weights are identical, but instead of measuring the outcome as treatment selection a(k), the outcome is an indicator variable for whether the patient remained in the study at time k.

Once the weights are known, one can apply a generalized estimating equation where observations are weighted by the product of the treatment selection and dropout stabilized weights.

This sounds too good to be true. What are the limitations of the MSM model? First, the MSM requires no unmeasured confounders. In other words, all variables that affect treatment assignment need to be included in the model for this approach to be valid. Second, there must be a positive probability for each treatment for each set of treatment history and covariates. Third, one must use the correct model structure when specifying the weights and analysis models. Finally, the data are assumed to be missing at random.

An example of the MSM approach was developed by Ng-Mak et al. (2019) as applied to patients with bipolar disorder who were treated with atypical antipsychotics.

There are many milestones that mark a coming of age. At 16 you can get your driver’s license, at 18 you’re a legally an adult and most kids then graduate high school and head off to college.

Just like these milestones, there are also several key dental milestones. Your parents remember your first tooth erupting (and the many more that came after), the first tooth you lost, any orthodontic work you had done, and finally getting your wisdom teeth removed.

For the younger generations, most of us remember getting our wisdom teeth out over summer break or between semesters in college. However, removing wisdom teeth hasn’t always been standard. In fact, one common question we get from our older patients who still have their wisdom teeth is if we still need to remove them. Just like with your appendix, wisdom teeth are fine to have until something goes wrong or a risk is identified. And when that happens, it normally requires immediate action.

If you still have your wisdom teeth, it’s important to discuss them with your dentist and determine if they could be doing more harm than good.

Why do we have wisdom teeth?

Sometimes more accurately referred to as our third set of molars, wisdom teeth were necessary once upon a time when our ancestors subsisted on a diet that consisted of tough meats and fibrous roots. In addition, these ancestors had much larger mouths, which could easily fit 32 teeth.

However, as humans evolved and we left the hunter and gatherer lifestyle, our jaws also changed. Thanks to softer foods and more diverse diets, we no longer needed an extra set of molars to help break down food. And with a smaller jaw, 32 teeth could no longer fit properly. Due to this, complications have become common, like teeth that don’t fully erupt and become impacted. Pain and infection always follow.

How did wisdom teeth get their name?

Third molars have been referred to as “teeth of wisdom” since the 17th century and just as “wisdom teeth” since the 19th century. These third molars generally appear much later than other teeth, usually between the ages of 17 and 25 when a person reaches adulthood. It’s generally thought today that they’re called wisdom teeth because they appear so late, at an age when a person matures into adulthood and is “wiser” than when other teeth have erupted. We won’t comment on the “wise” nature of 17 to 25-year-olds, but we’ll agree that these late-erupters definitely come at a later stage of life.

I’m an adult and still have my wisdom teeth, now what?

Dentists and oral surgeons don’t recommend removal just so we have something to do! Instead, we see the problem with wisdom teeth when there is no longer room for them in the mouth, resulting in poor root quality and oddly-shaped or angled teeth. Even if you do have the space in your mouth, there is a higher likelihood that your wisdom teeth could become infected or lead to the development of other periodontal diseases since they’re so far back in the mouth and that much harder to clean. Many times, pulling wisdom teeth is a preventative measure that is done to protect the long-term health of your mouth.

While there is no “correct” time for wisdom tooth removal, the younger you have it done, the easier the healing process. The procedure to remove wisdom teeth varies from patient to patient since sometimes the teeth are impacted or a patient may not have a full set. The procedure shouldn’t be painful with the correct anesthesia, and is almost always done in an outpatient setting. Proper care after the procedure is important to prevent painful side effects like dry sockets.

Removal prior to wisdom teeth causing a problem or resulting in more significant dental work is important. If you or your child still have wisdom teeth and you are looking for a consultation, give our office in Fort Worth a call today!

The post The History of Wisdom Teeth appeared first on Fort Worth Dentist | 7th Street District | H. Peter Ku, D.D.S. PA.

When you think “genomics,” your mind probably pictures a human DNA strand. Well, my mind did, prior to meeting with Dr. Joseph Frassica and Dr. Felix Baader at HIMSS19 to discuss Philips’ approach to the tragic problem of healthcare-acquired infections that kill patients. Ever since that conversation, my mind’s eye is filled with images of MRSA cells like those shown here.

When you think “genomics,” your mind probably pictures a human DNA strand. Well, my mind did, prior to meeting with Dr. Joseph Frassica and Dr. Felix Baader at HIMSS19 to discuss Philips’ approach to the tragic problem of healthcare-acquired infections that kill patients. Ever since that conversation, my mind’s eye is filled with images of MRSA cells like those shown here.

At HIMSS19, Philips launched a solution that couples clinical informatics with genomic sequencing of bacteria to quickly identify and treat patients that are affected with tough-to-treat infections that, so often, result in death.

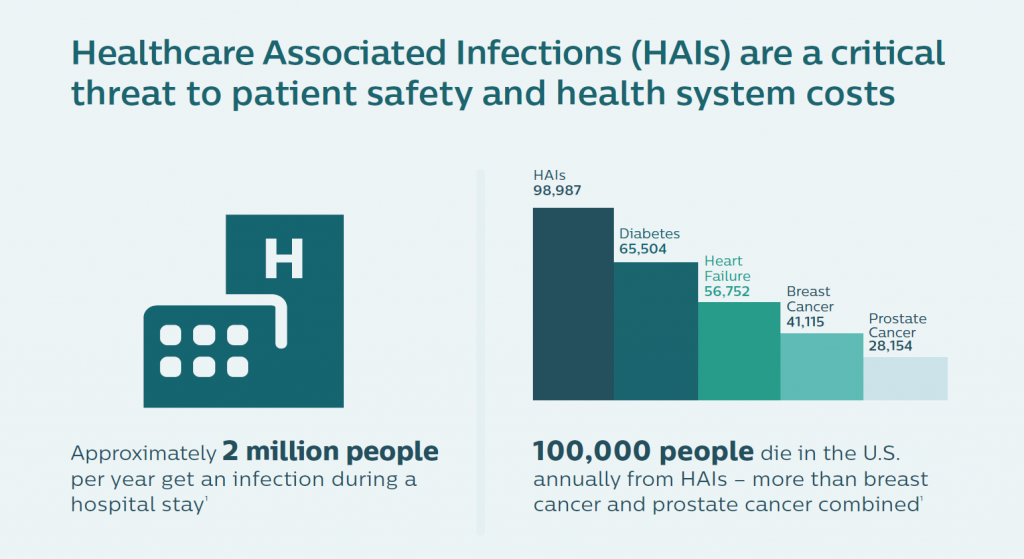

Healthcare-acquired infections (HAIs) are a worldwide challenge of epidemic, public health proportions. The World Health Organization recognizes that HAIs are a problem in both wealthy and developing countries. About 2.5 million Europeans die or are seriously debilitated each year from an HAI.

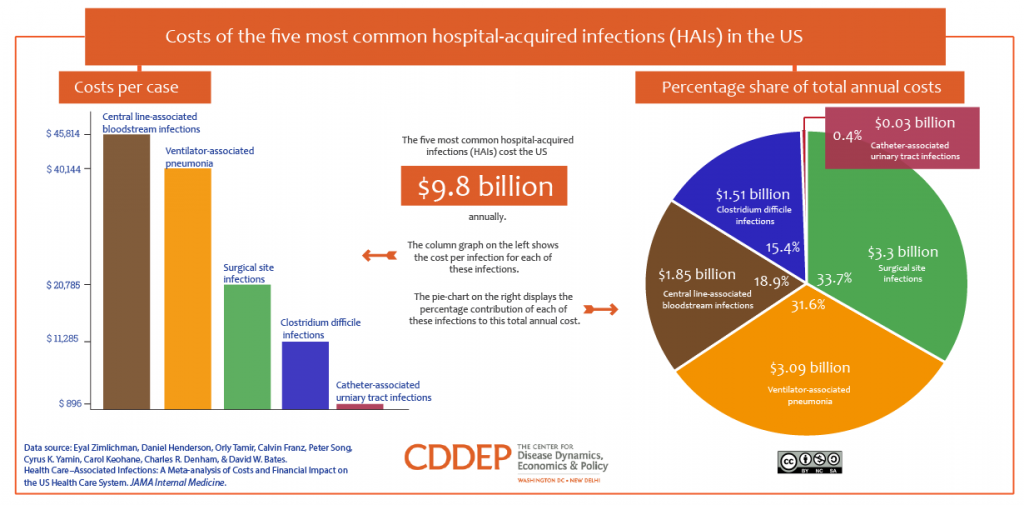

In the U.S., the five most common HAIs in the U.S. cost nearly $10 billion annually, according to an economic analysis published in JAMA Internal Medicine. More importantly, HAIs result in as many as 100,000 deaths a year in America. While the Leapfrog Group has recognized that U.S. hospitals have been working to improve the rate of nosocomial infections in America, there is a long way to go. One in 25 patients in U.S. hospitals still contracts an HAI, the Group’s recent report on HAIs attested.

Combating these deaths is a “winnable battle,” the U.S. Centers for Disease Control (CDC) believes. The lives that succumb to HAIs are cut short for reasons that are largely preventable. The researchers at Philips agreed with that sentiment, and worked to develop an approach to stem this crisis.

Philips’ solution marries informatics with genomics — leveraging two of the company’s key competencies. First, consider the informatics pillar, beginning with the many places and people where an infection can live: with a patient, a doctor, a nurse, a health aide; and, in an operating room, in an ICU, with a piece of surgical equipment, on an implement in the hospital cafeteria, for example. Now, digitally track that information through the patient’s journey during a hospital stay.

Second, deploy the skills to “genetically fingerprint pathogens,” the bacteria found in healthcare settings. It is now possible and increasingly cost-effective to do whole genome sequencing of pathogens in hospitals. The cost of doing so has fallen to the point where this approach to managing nosocomial outbreaks in large community hospitals is more feasible.

For the research on which the eventual tool was based, the Philips team members worked collaboratively and globally, across time zones, with healthcare customers. I learned details about the research done in collaboration with the Westchester Medical Center in Valhalla, NY, an organization that has been firmly focused on reducing HAIs. Working iteratively on concepts over time, the project yielded solid proof points proving out the solution: the time to detect an outbreak fell by 85%, and the process also revealed many more pathogens than would otherwise be identified: 20 unrecognized ones versus four.

For the research on which the eventual tool was based, the Philips team members worked collaboratively and globally, across time zones, with healthcare customers. I learned details about the research done in collaboration with the Westchester Medical Center in Valhalla, NY, an organization that has been firmly focused on reducing HAIs. Working iteratively on concepts over time, the project yielded solid proof points proving out the solution: the time to detect an outbreak fell by 85%, and the process also revealed many more pathogens than would otherwise be identified: 20 unrecognized ones versus four.

“We build the family tree of the infections,” Dr. Baader explained. “If you have that, you know what the parent and siblings of each bacterium is. If there’s a parent and sibling, we can identify a transmission” of the bacteria to a patient or provider. Through machine learning and algorithms, using the data described in the informatics data flow, the clinical team can figure out whether the transmission was from a device, a patient in a shared room, or a caregiver.

The solution saves time and enhances workflow and productivity: typically for this process, it would take six practitioners to review the massive data set of 150,000 possible connections in the network between patients. The Philips IntelliSpace Epidemiology Solution narrowed this down to 40 transmission events.

“The interesting thing is that this sounds like rocket science to sequence a bacterium,” Dr. Frassica explained. “But that technology has progressed in the last few years. The sequencing step can be done for $180 today. Our pilot site at Westchester Valhalla sequenced each and every sample, demonstrating that the cost of sequencing for bacteria is less than the standard workflow cost of doing a bacterial culture.”

“The interesting thing is that this sounds like rocket science to sequence a bacterium,” Dr. Frassica explained. “But that technology has progressed in the last few years. The sequencing step can be done for $180 today. Our pilot site at Westchester Valhalla sequenced each and every sample, demonstrating that the cost of sequencing for bacteria is less than the standard workflow cost of doing a bacterial culture.”

Dr. Frassica, a pediatric intensivist by training, put this cost-effectiveness into a public health cost-benefit context. “There are more deaths from HAI infection than from breast and prostate cancer combined,” he noted, further saying that genome sequencing bacteria also allows the hospital to know when the situation is not an outbreak. Without the real-time information and insights, “You might be tempted to close the unit and move patients. In some cases, things that looked suspicious were not HAIs. They were genomically so far apart they couldn’t be acquired infections.” The key data point here was that at Westchester Medical Center, out of 20 scenarios, three were not HAIs. So the hospital management didn’t have to close beds, conserving that opportunity cost in those cases.

For more information, here’s Philips’ press release on the program.

Health Populi’s Hot Points: The public health and regional population health benefit to this informatics/genomics approach to managing HAIs is clear. Philips is taking a similar approach in oncology, announcing that development at HIMSS19 as well.

The public health implications are personal to me, having lost a family member to a runaway infection acquired in a hospital many years ago. I get the value of this tool from both the personal perspective and through my broader professional and public health economics lens.

There’s another aspect to learn from here, too, via the design approach taken by the Philips team. Dr. Frassica shared a “then” and “now” perspective: in the past decade, the team would, “ask a bunch of people what they needed,” translate that input into “what we thought they needed,” and then bring the client a solution.

“Now” for the HAI research, “we bring collaborators in for ideation and iteration throughout the process of creating the product,” Dr. Frassica described. “We iterated this product continuously with our partners” at Westchester and with other partner health care providers for feedback.

Why? “To make these products function in the real world,” Dr. Frassica asserted.

Such a co-creation strategy is the way forward to innovating technology that helps make health care better for both providers and patients — and save lives in the process.

The post How Genomics Can Battle Killer Bacterial Infections in the Hospital – Talking With Philips at HIMSS19 appeared first on HealthPopuli.com.

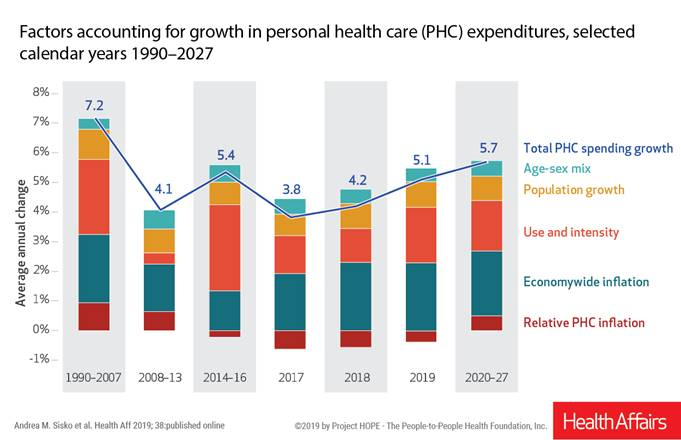

National health spending in the U.S. is expected to grow by 5.7% every year from 2020 to 2027, the actuaries at the Centers for Medicare and Medicaid Services forecast in their report, National Health Expenditure Projections, 2018-2927: Economic And Demographic Trends Drive Spending And Enrollment Growth, published yesterday by Health Affairs.

National health spending in the U.S. is expected to grow by 5.7% every year from 2020 to 2027, the actuaries at the Centers for Medicare and Medicaid Services forecast in their report, National Health Expenditure Projections, 2018-2927: Economic And Demographic Trends Drive Spending And Enrollment Growth, published yesterday by Health Affairs.

For context, note that general price inflation in the U.S. was 1.6% for the 12 months ending January 2019 according to the U.S. Bureau of Labor Statistics.

This growth rate for health care costs exceeds every period measured since the high of 7.2% recorded in 1990-2007.

The bar chart illustrates the factors contributing to growth in personal health care spending. The largest components are expected to be economy-wide inflation, utilization, and population growth.

Underneath this macro trend are some important trends to call out. A key headline is that there will be a shift expected from the commercially insured population to Medicare, as more Baby Boomers move from working health citizens to aging into Medicare. For these enrollees, increases in fee-for-service hospital care and prescription drugs will push spending upward.

In addition, five States are expected to expand Medicaid in the next couple of years, moving more people into these State-specific health insurance plans in Idaho, Maine, Nebraska, Utah and Virginia. (These are the known-knowns of Medicaid expansion at the time CMS published this forecast).

The cost driver of “use and intensity” responds to these covered populations and people gain access to insurance and, therefore, services. The share of health care spending sponsored/financed by Federal, State and local governments will grow to 2027, reaching 47%. Thus, by 2027, health spending will be roughly split by public and private sector sources of payment.

Growth in prescription drug spending is another area to watch in this forecast, and others we track on Health Populi. CMS expects Rx drug spending to increase by 6.1% year on year to 2027, accelerated growth due to aging of the population and new more expensive drugs expected to come onto the market to treat cancer, diabetes, and Alzheimer’s disease, among other treatments. (For more on specialty drug cost growth, see this post in Health Populi).

Keep in mind the methodology of this annual forecast: CMS actuaries do not anticipate or design in sensitivity analysis for any changes to workflow, plan design (like value-based bundled payments), or consumer behavior change. Market-based wild cards, such as consumers’ conducting more medical visits via lower-cost telehealth channels (to lower costs), or growing adoption of financial support for high-cost medicines (such as Bluebird Therapeutics’ vision to charge a patient based on an installment plan and outcomes over a course of years using a therapy) could move these numbers up or down.

Health Populi’s Hot Points: By 2027, $1 in every $5 of the GDP will be spent on health care in America. The aging of America, combined with very expensive novel treatments coming on stream to deal with both chronic condition epidemics like diabetes and heart disease, and to treat complex conditions like Parkinson’s, Alzheimer’s, HIV/AIDS, and once-untreatable cancers.

Most Americans are coming to embrace and expect health care as a civil right through some form of universal health insurance in the U.S. Many of the candidates who have come forward to run as Democratic candidates for President support some flavor of Medicare for All, one of many possible designs for universal health care in America.

As Medicare enrollment organically grows based on current demographics in the nation, the health plan will be challenged to meet its fiscal obligations based just on its current actuarial expectations. The 19.4% GDP share for health care expected in 2027 based on CMS’s current projections of the current state would shift well above 20% were Americans, say over 50 years of age, allowed to buy into Medicare as envisioned by some of the Presidential candidates’ platforms for health care reform.

We’ll continue to track the growing embrace of universal health care tempered by the health economic and macroeconomic realities in the coming months leading up to the 2020 U.S. Presidential Election. Many grassroots health care issues will play into this discussion, from the cost of EpiPen for middle-class families, to access for specialty drugs that treat a child’s leukemia (running over $500,000 for CAR-T therapy, as an example) to a senior’s need for a ride to a medical appointment — falling into the crucial bucket of social determinants that bolster public and individual health.

For now, the sobering state of affairs is that in America, health care costs continue to increase faster than the rest of the economy, and economic growth overall.

The post National Health Spending Will Reach Nearly 20% of U.S. GDP By 2027 appeared first on HealthPopuli.com.

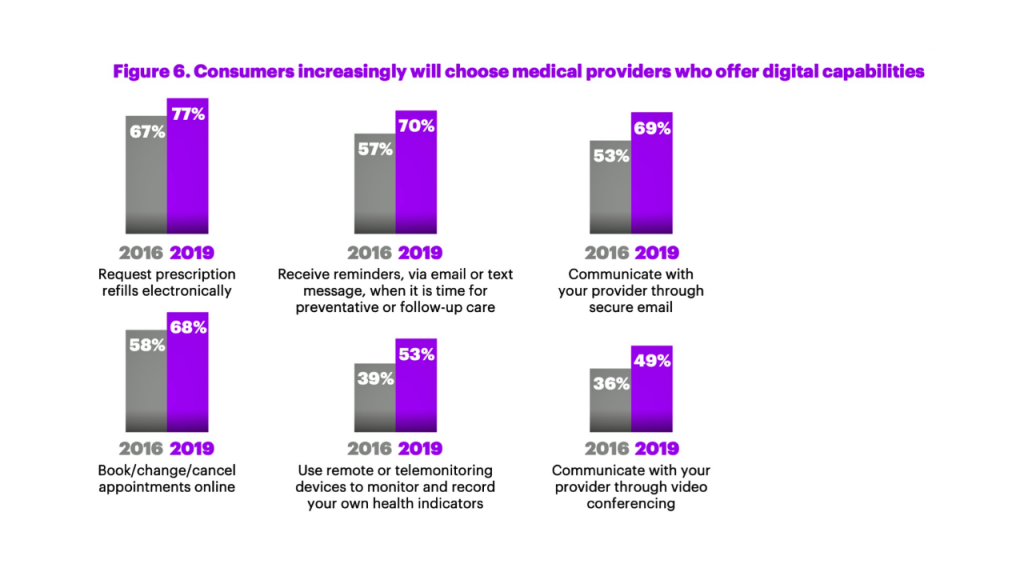

![]() Across generations, from younger to older patients, cost, transparency and convenience drive consumer satisfaction, Accenture’s latest health consumer survey found.

Across generations, from younger to older patients, cost, transparency and convenience drive consumer satisfaction, Accenture’s latest health consumer survey found.

I had the opportunity to brainstorm the study’s findings in real-time on the day of survey launch, 12 February, with Dr. Kaveh Safavi, Brian Kalis, and Jenn Francis at HIMSS19. Our starting point was the tipping-point statistic that over 50% of people in the U.S. have chosen to use a non-traditional health care setting. Those non-traditional sites of care include walk-in and retail clinics, outpatient surgery centers, virtual health (whether on the phone, on video or via mobile apps), on-demand services, and digital therapeutics.

We weren’t surprised to note that younger patients took advantage of retail clinics and other on-demand channels for health care, older people, too, have been willing to use sites other than doctor’s offices and hospital clinics to receive health care services.

Accenture has conducted research among health consumers for several years, so we could compare 2016 to 2019. In 2016, one-half of people said they would choose a doctor based on digital capabilities. In 2019, that digital health preference reached three-fourths of consumers, “a step function increase,” Kaveh noted. “Expectations for digital enablement is moving into the mainstream,” he observed.

Accenture has conducted research among health consumers for several years, so we could compare 2016 to 2019. In 2016, one-half of people said they would choose a doctor based on digital capabilities. In 2019, that digital health preference reached three-fourths of consumers, “a step function increase,” Kaveh noted. “Expectations for digital enablement is moving into the mainstream,” he observed.

People in middle-age tend to behave more like their kids than older parents. This is driving choice when patients select which health care system to work with, Brian explained. There’s a higher preference for systems with richer digital capabilities.

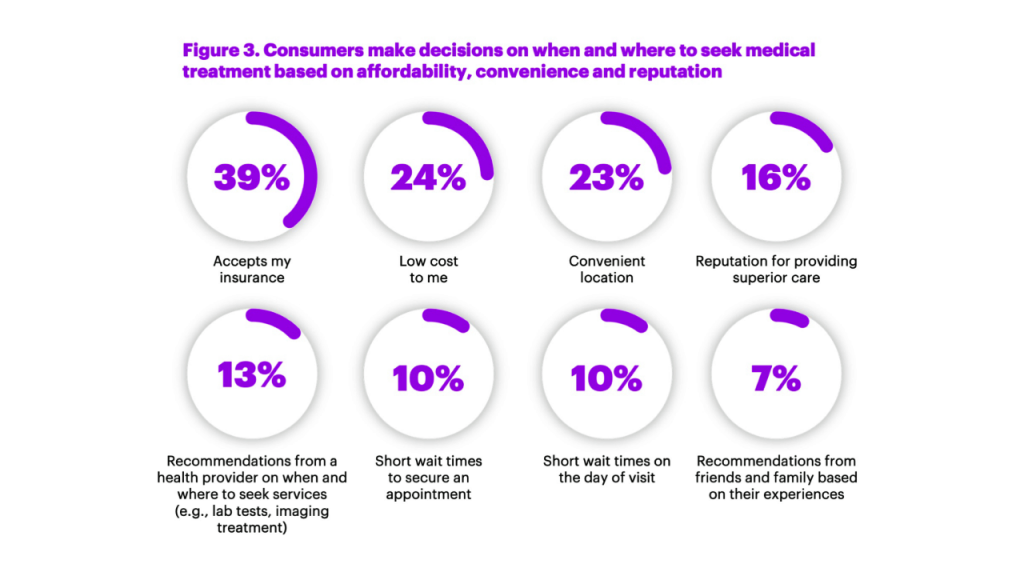

Beyond the digital convenience and life-flow streamlining, consumers are willing to go to alternative settings based on cost — where the alternative health provider site accepts “my” insurance, thus lowering my out-of-pocket cost — and convenient location, which was three-times more important than recommendations from friends and family.

In past studies, such word-of-mouth from “people like me” has been a top driver of consumer health care decision-making.

Understanding “my” personal costs in advance of treatment, and greater price transparency, are part of this thinking and expectation.

Understanding “my” personal costs in advance of treatment, and greater price transparency, are part of this thinking and expectation.

When consumers select a non-traditional site for health services, they are generally seeking care for respiratory conditions, physical injury, aches and sprains, and pediatric care for their children.

We’ve also begun to see specialization in non-traditional settings, such as orthopedic urgent care and allergy centers emerging to address niche needs.

Health systems are re-imagining care beyond the bricks-and-mortar institution, Brian commented. In local communities, health care providers recognize the need to meet consumers closer to home, work and play, to reach and engage patients digitally and physically redefining the “front door” to health care.

This led us to a discussion of how the electronic health record could reach into these more retail health locations, especially challenging if not directly owned by the health system. The big announcement from CMS via Seema Verma during HIMSS19 addressed open data and standards that would help make data more liquid and interoperable, highly relevant to this situation of care in the community in places that may or may not be owned by a patient’s health system. Collaboration for health care in the community, for services and for social determinants of health factors, is a growing feature in U.S. health care — and desirable. But collaboration with added fragmentation is not a success factor for quality patient care, outcomes, and cost-effectiveness.

“Digital is not a discrete thing on the side,” Brian asserted. “The entire mindset [in health care] is changing the way you do all your business, not ‘in addition.'”

For this study, Accenture polled 2,338 U.S. healthcare consumers 18 and over in November and December 2018.

Health Populi’s Hot Points: Patients, now consumers and ultimately payors managing up to their deductible and out-of-pocket health care costs, are clearly seeking health care services on their terms — based on value and personal values. That’s the demand side. On the supply side, we see CVS and Walgreens both announcing new concepts in retail health morphing what our idea of a “pharmacy” is well beyond dispensing prescription drugs.

Health Populi’s Hot Points: Patients, now consumers and ultimately payors managing up to their deductible and out-of-pocket health care costs, are clearly seeking health care services on their terms — based on value and personal values. That’s the demand side. On the supply side, we see CVS and Walgreens both announcing new concepts in retail health morphing what our idea of a “pharmacy” is well beyond dispensing prescription drugs.

Whether the CVS “HealthHUB” or Walgreens addition of dental, telehealth and vision services, the new health consumer-payor will increasingly find services closer to home for both non-acute medical needs and chronic condition management. Walmart, another key channel in the expanding retail health landscape, just announced that they will extend telehealth visits to employees for the low-low cost of $4 (yes, you read that correctly).

To get this right, it can’t just be about new locations for lower-cost services, even at a high degree of consumer confidence and supplier quality. The person’s/patient’s data from these encounters experienced quite apart (physically) from a patient’s health care system must find their way to a person’s health record. This is the promise of the CMS announcement, which is seeking input from interested health care stakeholders. Here’s the link: let’s opine and ensure we add no more fragmentation to our all-too-fragmented health services landscape.

The post Cost and Convenience Underpin Patient Demands As Health Consumers appeared first on HealthPopuli.com.

Seeking health information online along with researching other patients’ perspectives on doctors are now as common as booking dinner reservations and reading restaurant reviews, based on Rock Health’s latest health consumer survey, Beyond Wellness for the Healthy: Digital Health Consumer Adoption 2018.

![]() Rock Health has gauged consumes’ digital health adoption fo a few years, showing year-on-year growth for “Googling” health information, seeking peer patients’ physician and hospital reviews, tracking activity, donning wearable tech, and engaging in live telehealth consultations with providers, as the first chart shows.

Rock Health has gauged consumes’ digital health adoption fo a few years, showing year-on-year growth for “Googling” health information, seeking peer patients’ physician and hospital reviews, tracking activity, donning wearable tech, and engaging in live telehealth consultations with providers, as the first chart shows.

The growth of tracking and wearable tech is moving toward more medical applications beyond fitness and wellness, Rock Health found. This is due to more tools gathering more clinical evidence to show effectiveness and validity. Some innovators have invested the time and money to undergo FDA clearance; some have collaborated with health care providers and researchers to build evidence cases and calculate cost-effectiveness or ROI for their use.

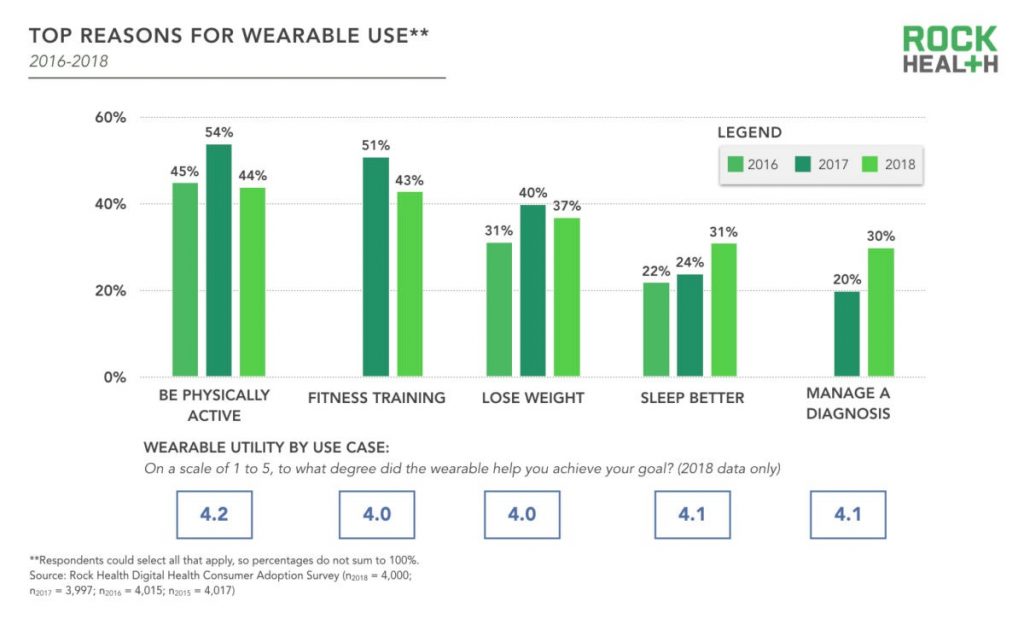

While fitness training and bolstering physical activity have lost traction by ten points each, the second bar chart illustrates, managing a diagnosis and sleeping better have gained consumer traction. Rock Health analysts expect that wearable tech use will continue to grow with more use cases for remote health monitoring coupled with consumers and patients being incentivized to continue their use.

While fitness training and bolstering physical activity have lost traction by ten points each, the second bar chart illustrates, managing a diagnosis and sleeping better have gained consumer traction. Rock Health analysts expect that wearable tech use will continue to grow with more use cases for remote health monitoring coupled with consumers and patients being incentivized to continue their use.

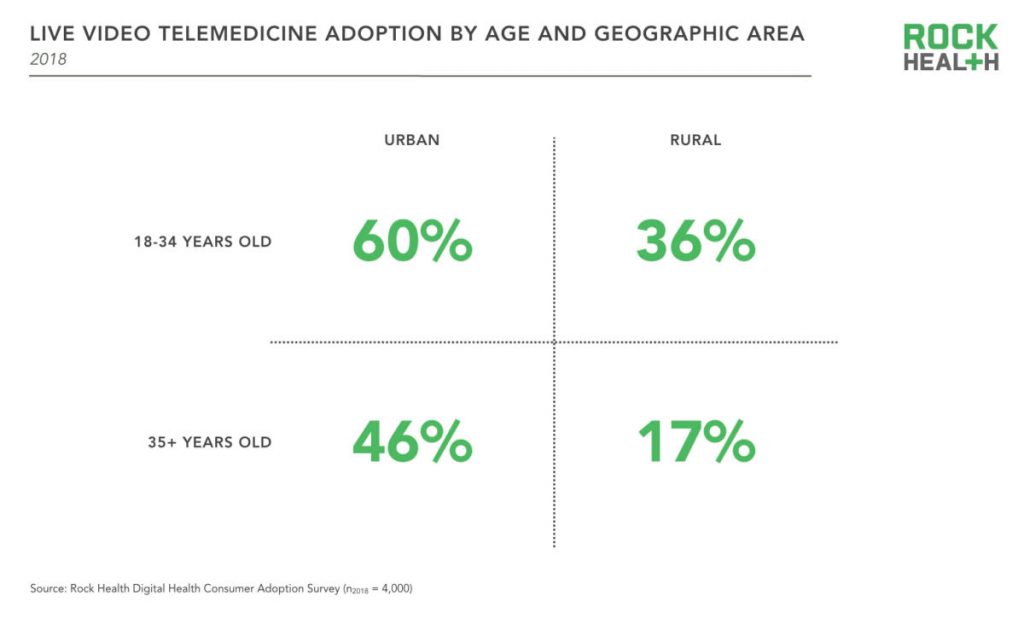

Telehealth adoption also grew from 2017 to 2018. I discussed the supply and demand sides of telehealth converging based on my conversations at HIMSS last week (my observation: that telehealth is morphing into, simply, health care workflow). The biggest growth, Rock Health found, was for live phone telehealth, with 64% of respondents using this channel, followed by email and text. Live video use roughly doubled, from 19% in 2017 to 34% in 2018.

Life video telehealth adoption was most prominent among younger patients, 18 to 34, living in urban geographies.

Trust continues to be the most important precursor to health engagement, we learned in the Edelman Health Engagement Barometer, and Rock Health notes this to still be the case. “My physician” is the most trusted data steward, with 72% of consumers willing to share health data with “their” personal doctors. Tech companies? Only 11% of consumers said in 2018 that they’d be willing to share health data with them. Within that 11% marginal interest, the top-ranked tech companies for sharing were Google, Amazon, and Microsoft, each with over 50% of interest; Apple garnered 49% of that 11% trusting tech. FYI, Facebook had 40%, and IBM, 34%.

Physicians increasingly understand and appreciate the trust equity they’ve earned with patients. To continue to nurture that precious asset, JAMA published this article last week on A Framework for Increasing Trust Between Patients and the Organizations That Care for Them. The key takeaway: “No single approach will ensure, maintain, or rebuild trust. There is important work to do by payers, boards, senior management, middle management, and clinicians. The key themes that emerged from this work group included commitment to meeting patients’ needs as the core of organizational culture; measurement of patients’ experience and clinician engagement; creation of systems of accountability with financial and nonfinancial incentives; building of effective teams; cultivation of communication and relationship skills; and inclusion of patients in all phases of this work.”

Health Populi’s Hot Points: The health consumer conundrum on trust and “my” health/care data in our current world is that so much health-related data isn’t covered by HIPAA or in the medical claim or EHR. Some of the most impactful and insightful consumer information is mashed up from retail receipts, fast food check-ins, and mobile phone use and GPS sitings.

Health Populi’s Hot Points: The health consumer conundrum on trust and “my” health/care data in our current world is that so much health-related data isn’t covered by HIPAA or in the medical claim or EHR. Some of the most impactful and insightful consumer information is mashed up from retail receipts, fast food check-ins, and mobile phone use and GPS sitings.

At HIMSS19 last week, we noted a growing cadre of service organizations like Acxiom, LexisNexis, and TransUnion who play various roles in profiling patients as consumers and payors. Rock Health is right to note consumers’ concerns about privacy and security of “my” data in the post-Facebook/Cambridge Analytica environment. I wrote about this exactly one year ago after HIMSS18…forecasting this point on the minds of health consumers.

In the U.S., patients-as-consumers-as-payors aren’t well served by HIPAA, which was written in the pre-smartphone, medical breach era.

I’m encouraged to see that Americans are growing in knowledge and awareness of privacy threats and the value of personal information demonstrated by this last graph from the Rock Health survey. Awareness of health data privacy is an important aspect of health literacy. Will patients-as-voters in the USA express their demands for better privacy protections as health citizens? That is my yet-to-be-answered question.

The post Open Table for Health: Patients Are Online For Health Search and Physician Reviews appeared first on HealthPopuli.com.

Devin Incerti does not blog much; only about 7 times in 4 years. When he does, however, it’s worth paying attention. For instance, he has put together a super helpful blog post describing how to do probabilistic sensitivity analysis (PSA) in R. A key feature of any PSA is determining the distribution from which one makes draws for different parameter values. Dr. Incerti–my colleague at PHE–gives some helpful pointers of how to use the following distributions:

Dr. Incerti’s blog post also describes how to preform a PSA, and has R code describing how to create these distributions. There are also a lot of helpful graphs as well.

Have you heard that February is National Children’s Dental Month?

That means it’s the perfect opportunity to highlight one of our favorite social media influencers we follow on Twitter: the American Academy of Pediatric Dentistry.

If you have little ones in the house or are just curious about best practices for children and their teeth, then follow along at @AmerAcadPedDent for unique insight and one-of-a-kind tips.

Below are some of our favorite tips provided by the American Academy of Pediatric Dentistry. If you have a child or know someone who is looking for a dentist, then give Dr. Ku’s office today! We love working with your family—including down to the littlest ones!

Some of our favorite tweets from major dental influencers this month:

Ensuring your children are healthy starts in the womb. While most women assume this means eating healthy, taking vitamins and getting enough rest, it also includes ensuring optimal oral health. Women who have cavities when they are pregnant can pass the bacteria that causes them along to their children, and gum disease can lead to premature birth or low birth weight.

If you have kids, then you know that they always seem to have an accident at a time when you can’t reach your doctor or dentist. And as we head into the warmer months (which means more play time outdoors and a higher potential for injury), the American Academy of Pediatric Dentistry provided an easy-to-read overview on what to do in the event of a tooth that is knocked out, a chipped tooth, or excessive bleeding.

This post speaks to something we wholeheartedly believe at Dr. Ku’s office, and which is why we are committed to providing excellent care to even our smallest patients.

Maybe this is why we were named the number-one dentist in Fort Worth by the Fort Worth Star Telegram for the second year in a row.

Creating a dental home for your child creates a familiarity which helps decrease dental anxiety and promote openness.

When it comes to something as important as your kids’ teeth, parents want to take charge to ensure that everything’s done properly. However, while supervision is important, it is also good to teach being self-sufficiency. This tweet provides a good metric for when your child is ready to floss on their own teeth. When it comes to brushing, you can start even earlier. Let your toddler practice brushing their teeth and then make sure you come in and finish up for them. Creating the habit early will ensure good, lifelong habits.

As a parent, you have definitely thought about the time missed at school for common maladies like a cold or flu. But children are also suffering from severe oral health problems and missing significant amounts of school, too. Just like good hand washing prevents colds, good preventive oral health helps prevent more severe oral health issues like tooth decay, gingivitis or gum disease. Each of these issues can strike children just as they do adults.

In addition to this wide range of tips and tricks for parents, the American Academy of Pediatric Dentistry offers opportunities for continuing education that help keep our practice on the cutting edge. If you have any questions about how we serve children in Fort Worth, then give our office a call today!

The post Dental Influencers You Should Follow appeared first on Fort Worth Dentist | 7th Street District | H. Peter Ku, D.D.S. PA.

The answer appears to be ‘yes’ according to a survey by Mahendraratnam et al. (2019). After surveying subject matter experts that were senior representatives from payer organizations and pharmaceutical manufacturers on value-based pricing arrangements (VBA), they found:

More than 70% of VBAs implemented between 2014 and 2017 were not publicly disclosed. Furthermore, although consideration of VBAs as a coverage and payment tool is increasing, VBA implementation is relatively low, with manufacturers and payers reporting that approximately 33% and 60% of early dialogues translate into signed VBA contracts, respectively.

In short, VBAs are more common than we thought, but still not that common overall.

Ten years ago, two brothers, physicians both, started up a telemedicine company called American Well. They launched their service first in Hawaii, where long distances and remote island living challenged the supply and demand sides of health care providers and patients alike.

It’s ten years later, and I sat down for a “what’s new?” chat with Roy Schoenberg, American Well President and CEO. In full transparency, I enjoy and appreciate the opportunity to meet with Roy (or very occasionally Ido, the co-founding brother-other-half) every year at HIMSS and sometimes at CES. In our face-to-face brainstorm this week, we covered a wide range of topics, starting with some historical context to get to the “new and now.”

That launch of AmWell in Hawaii was with a payer, a unit of Blue Cross. The company’s early bet and first strategic choice was to work with payers. That segment is a significant business now, Roy explained. The company works with virtually every major payer-player, and 45 Blue Cross Blue Shield plans as well. This is a core business for AmWell.

The company’s second strategic choice was to “put the technology in others’ hands,” Roy described, with AmWell’s services, “baked into other businesses.” Doing so in this way could help health/care ecosystem stakeholders to innovate their own business and pricing models. AmWell invested in making their own technology easier to tie into other businesses’ infrastructures and architectures. Consider the plethora of EHR systems, scheduling idiosyncrasies, physician adoption and workflow considerations, and patient matching challenges, for example.

On the health system (provider) side, there is substantial pressure to reduce costs and at the same time, provide innovative services. These services are increasingly ambulatory and mobile, based on both cost and consumer preferences. AmWell’s customers cover about 150 million lives. Don’t mistake that for “reach,” Roy warned me when I quickly calculated, “So, you reach 50% of the U.S. population.” It’s a potential consumer/patient market that AmWell could serve, but not every person with access to telehealth services takes advantage of that supply side.

Remember the Field of Dreams effect? “If you build it, they will come?” In telehealth, even with employers covering the service as a workplace benefit, most employees still don’t “benefit from the benefit.” We discussed this disconnect on our panel today at HIMSS19, addressing digital traction in consumerization of health care.

Dr. Peter Rasmussen explained that there are many reasons consumers don’t yet engage in virtual health services. In some systems, like Kaiser-Permanente, at least 50% of encounters are done via non-traditional channels: via secure email with clinicians, via video chat, and asynchronous chat, for example. Intermountain and Mercy Virtual, too, conduct lots of visits via telehealth means. However, some recent market research estimates have identified very low, single digit consumer market adoption.

A major limiting obstacle for providers has been licensure, where a doctor peer of Peter’s in Cleveland cannot provide a second opinion for a patient in rural Kentucky for a rare cancer due to the Ohio physician’s lack of license in the Bluegrass State. I noted that in the EU, this isn’t a problem for physicians operating in different countries, from the far north to the Mediterranean south.

On the consumer side, a Jetsons-style telehealth visit with a clinician on a screen can seem too Star Trek tricordery, whether small on a phone or on a large-screen PC monitor. But once a patient-consumer experiences that virtual visit, most people want to repeat the telehealth encounter. Here, Jane Jetson is very happy to be able to access a telehealth visit for her son, Elroy — and true enough, back here in the digital health Stone Age, Moms with young children are particularly keen on virtual visits especially on nights and weekends.

To smooth organizations’ way to offer telehealth, American Well offers an SDK, a software development kit. This package drops into the client’s technology. Samsung, for example, build an American Well ap into their phone. New York Presbyterian Hospital has an app for telehealth from American Well. AmWell SDKs have also been used by Medtronic, Cerner, and Philips, among others. The Apple Heart Study used the SDK.

“American Well is like the Intel inside,” Roy agreed with my analogy.

In a new HIMSS19 announcement, Netsmart uses the AmWell SDK for a behavioral health opioid program, announced today.

On our panel today, Greg Orr from Walgreens, Jessica Gelzer from Heal, and Dr. Rasmussen of Cleveland Clinic discussed the blurring between the traditional physician and the newer digital side. In retail , this is happening, with the poster child of Amazon invoked at every health care meet-up over the past year and ongoing.

I believe this is “omnichannel” in retail, and it’s happening in health care deliery, too.

Roy’s Amazon-analogy pointed me to the concept of “inventory.” Amazon shows us that stuff doesn’t have to live on Amazon’s warehouse shelves. “You don’t need to own it, but to route it,” Roy explained.

So for that industry disruptor, the key tactic is to develop and implement skills around inventory distribution.

Thus, the quote in the title of this post: as Roy asserted, “telehealth is the distribution channel for health care services.”

And here’s the next money quote and lightbulb moment: “We have to let go; we can’t be the product.”

In sense of the services available in the “inventory,” those, too, have expanded since the start of offering a physician visit. Today, specialists are part of the AmWell physician network, as well as womeen’s health experts, nutrition counselors, weight loss coaches, lactation support, and the fast-growing area and need on the demand side for behavioral health.

Health Populi’s Hot Points: Live telemedicine visits are more prevalent among younger urban-dwelling consumers, with lower adoption among rural, older residents, Rock Health learned in its fourth and lattt digital health consumer survey.

This means that some of the very people who most need access to health care services — rural, older, frailer health citizens — aren’t tapping into virtual visits. As Dr. Rasmussen pointed out, there can be may reasons a person doesn’t engage in telehealth: cultural, financial, or trust/privacy. I would also add in the role of of connectivity and broadband as a social determinant of health, clearly a barrier to adoption in rural areas that can lack connection to the last mile, and to the last person/patient.

In the growing health ecosystem landscape of retail health for patients-as-payors, attending to social determinants of health is at least as important as paying attention to health care services and specialty care access. I expect that AmWell will expand its footprint and services from the nutrition and weight loss areas to other behavioral and social factors that play so integrally into peoples’ overall health and wellness.

At HIMSS19 we see some exhibitors that will support this kind of consumer engagement and ecosystem build-out: AWS (Amazon Web Services), Google, Microsoft (with announcements for the Azure cloud collaborating with Walgreens, for example), and Salesforce bringing CRM capabilities to health and social services.

Ten years from now — even three years from now — I cannot forecast what new-new collaborations and services Roy and I will talk about. I’m certainly doing scenario planning on this for my advisory work.

But of one thing I am sure: in that decade-away scenario, the home will certainly be the hub of health.

The post “Telehealth is a digital distribution channel for health care” – catching up with Roy Schoenberg, President and CEO of American Well appeared first on HealthPopuli.com.

Measuring treatment value is difficult. Costs are relatively easier to measure but benefits are often more difficult, particularly impact on caregiver burden, productivity, quality of life and other factors. Not only that, but the “benefits” that accrue to a person may vary by individual. Some individuals may prefer treatments that are more effective, but with more side effects; others may be willing to sacrifice some efficacy to avoid side effects.

In addition to those challenges, a treatment’s value–particularly its estimated value–change over time. Value changes when the price changes, but the estimated value also changes as we get new evidence to better understand cost and benefits from additional clinical trial information, real world data, surveys, and other data sources.

With that background, ICER has decided to evaluate treatments for unsupported price increases. Re-evaluating treatment value over time is an important challenge to address. For instance, the Innovation and Value Initiative does this by creating dynamic tools online and putting source code freely available online in order to allow model updates as new information becomes available. ICER has chosen to do report updates, which is less flexible, but a needed improvement to doing a single value assessment at one point in time.

With that as a backdrop, I was interviewed by PharmaLive to further discuss this topic.

According to Jason Shafrin, Ph.D….. “The value of a treatment changes over time based on the evidence available about its benefits, risks, and costs,” Shafrin says. “In fact, Dana Goldman and others have proposed a three-part pricing model, where drug prices start out relatively low and increase over time as uncertainty resolves, and then fall after patent expiration. A key question is, how do we determine when new evidence would justify price increases? Thus, ICER addresses a pressing issue.”…

Health economics and outcomes researchers have recommended the inclusion of nonclinical value assessments into HEOR such as a treatment’s effect on productivity, caregiver burden, educational outcomes, and other factors. “As this evidence accumulates, it is important for ICER to incorporate these components into its value assessment as well,” Shafrin notes. “My own research has shown that including these recommended components can significantly affect a treatment’s estimated value.”

“The promise of AI is undeniable…could AI help clinicians deliver better and more humanistic care?” This question is asked and answered in a JAMA viewpoint published January 1/8 2019 titled, Humanizing Artificial Intelligence.

This theme motivated a conversation held over a dinner convened by Philips hosted by Frans Van Houten this week at HIMSS19.

To provide context Geoff Colvin, Fortune‘s Senior Editor, first talked about taking friction out of industries, as Lyft and Uber have done in the transport sector. “Taking friction out of industries challenges and changes business models,” Georff noted. With Uber’s IPO valuation approaching $100 billion, I’d say that’s some business model.

To provide context Geoff Colvin, Fortune‘s Senior Editor, first talked about taking friction out of industries, as Lyft and Uber have done in the transport sector. “Taking friction out of industries challenges and changes business models,” Georff noted. With Uber’s IPO valuation approaching $100 billion, I’d say that’s some business model.

This is a phenomenon that has impact across all industries, where business model innovation is now a core competence for all sectors, Geoff said.

In healthcare it’s difficult to take friction out of such a complex and highly regulated industry. But with big problems come big opportunities.

Artificial intelligence, AI, is a huge theme at HIMSS19. It also has the potential of being an enormous boon to humanity, Geoff imagined. AI is the type of tool that economists (my own professional guild) refer to as a “general purpose technology” because it crosses all industries. THINK: electricity and the open Internet, for examples.

Organizations today are struggling with how to get a grip on AI and apply the tool in their businesses: where and how much to invest? What is the business case for AI in our enterprise right now? they ask.

Geoff said there’s one core truth to consider: that humans will be economically valuable to the extent they can use deep human interaction.

This is why AI may have the biggest impact on health care compared with other industries, he posited.

The human side of the AI/human interface is so valuable, particularly in health care: evidence shows that we have better health outcomes if the caregiver relationship is better, stronger, and resilient.

Now, consider the root problems that the Quadruple Aim addresses: drive health outcomes, enhance the health experience for both patient and provider to prevent burnout, and lower per capita medical costs.

In health/care, the real business we are in is a relationship business.

Geoff introduced Philips’ CEO, saying, “Frans made Philips a health care company.”

Geoff introduced Philips’ CEO, saying, “Frans made Philips a health care company.”

In his introductory remarks, Frans called out that health care is unaffordable. The system will face growing demands based on lifestyle-driven diseases and the natural course aging. Eventually, he said, the medical bill needs to be contained. This is a global challenge for health systems around the world, although a particularly unsustainable challenge for volume-driven fee-for-service payment in the U.S.

Combine that demand side on the consumer/patient side with the fact that pressures in health care delivery organizations are creating dissatisfaction among health care workers, a Bain study recently observed looking at the “front line of health care.”

That’s one leg of the 4-part Quadruple Aim stool: to enhance health care experience for both patients and providers. A burned-out clinician is not an ingredient for bolstering a resilient, high performing health system.

How? Frans asked.

He responded to his question: “Innovation must be purposeful for clients.” Philips invests $1.8 billion on R&D, using the lens of the Quadruple Aim to measure innovation by that definition. If the R&D spend on a particular area doesn’t score on the Quad-Aim metrics, “we are doing something wrong,” Frans believes. “We must embrace courage while avoiding unproductive tangents.”

Focusing in on AI, Frans described, “We are in a Valhalla of innovation where there are false starts…we’re on a learning curve regarding AI. We [prefer to] talk about ‘adaptive’ not ‘artificial’ intelligence.”

For new business models, we need to engage in “creative and brave conversations” with payors, providers and patients, Frans believes. That’s part of developing deep human interactions with stakeholders in health care. Getting into these discussions can yield rich insights: for example, better understanding and empathizing with the role of the patient-as-consumer-as-payer in the context of the hospital CFO’s challenges with revenue cycle management and collections, with social work’s concerns about continuity of care once the patient leaves the hospital, could result in a creative solution to provide rich and well-designed information at the time of discharge that surrounds the patient with a feeling of empowerment and engagement adapted for them.

Once home, if the patient engages in effective self-care, she can prevent a readmission which then can help the hospital conserve costs. “Saving 30% of costs would create the oxygen to do really interesting things,” Frans explained.

In this moment of AI fear and trepidation, Frans explained, “AI is often seen as an implied threat…but it doesn’t have to be a massive mystical threat….It won’t profoundly impact ‘tomorrow’ but is a reason to optimize operations today.”

Frans pointed us to a just-published article in Nature Medicine on using AI for more effectively diagnosing childhood diseases. The study mashed up 101.6 million data points from 1,362,559 pediatric patient visits to a health system. Various pediatric conditions assessed in the study are shown in this diagram from the study. The data model proved accurate compared with pediatricians diagnosing common childhood conditions.

Frans pointed us to a just-published article in Nature Medicine on using AI for more effectively diagnosing childhood diseases. The study mashed up 101.6 million data points from 1,362,559 pediatric patient visits to a health system. Various pediatric conditions assessed in the study are shown in this diagram from the study. The data model proved accurate compared with pediatricians diagnosing common childhood conditions.

AI won’t replace those pediatricians, but can enhance their diagnostic toolbox and also help scale care to under-served communities.

At the end of the day, the JAMA column on humanizing artificial intelligence concludes that, “Humans in need want the best of what science and medicine have to offer…Bettering the ability of physicians to truly care for and express caring is the challenge for colleagues in computer science and medical informatics….is it possible to invent and discover applications that can enhance the human abilities in clinicians to better engage in caring for hte patient?”

This was the intention of the Philips team in convening us to ponder the theme of leveraging 21st century technology to reinvent health care at HIMSS19. At this year’s conference, AI has been a major theme discussed in both education sessions and on the exhibit floor. We would be wise to embrace this humanistic approach to AI (whether we consider the “a” as artificial, adaptive, augmented, awesome or alarming). As consumers learn more about the promise of AI, they will also look to organizations to utilize AI in the context of corporate social responsibility and fair play.

The post Deep Human Interactions: The Antidote To More AI In Health Care – Learning From Philips’ CEO At HIMSS19 appeared first on HealthPopuli.com.

Just as we experienced “e-business” departments blurring into ecommerce and everyday business processes, so is “telehealth” morphing into, simply, health care delivery as one of many channels and platforms.

Telehealth and virtual care are key education topics and exhibitor presences at HIMSS19.

Telehealth and virtual care are key education topics and exhibitor presences at HIMSS19.

Several factors underpin the adoption of telehealth in 2019:

Nearly all health care providers plan to expand existing on-demand virtual care services, with 6 in 10 of them planning to do so in the first half of 2019, Zipnosis learned in a benchmarking survey that polled 56 organizations operating in all 50 U.S. states.

Nearly all health care providers plan to expand existing on-demand virtual care services, with 6 in 10 of them planning to do so in the first half of 2019, Zipnosis learned in a benchmarking survey that polled 56 organizations operating in all 50 U.S. states.

Of those already offering virtual care services, about 50% have been operating for under 3 years, and one-third, over five years.

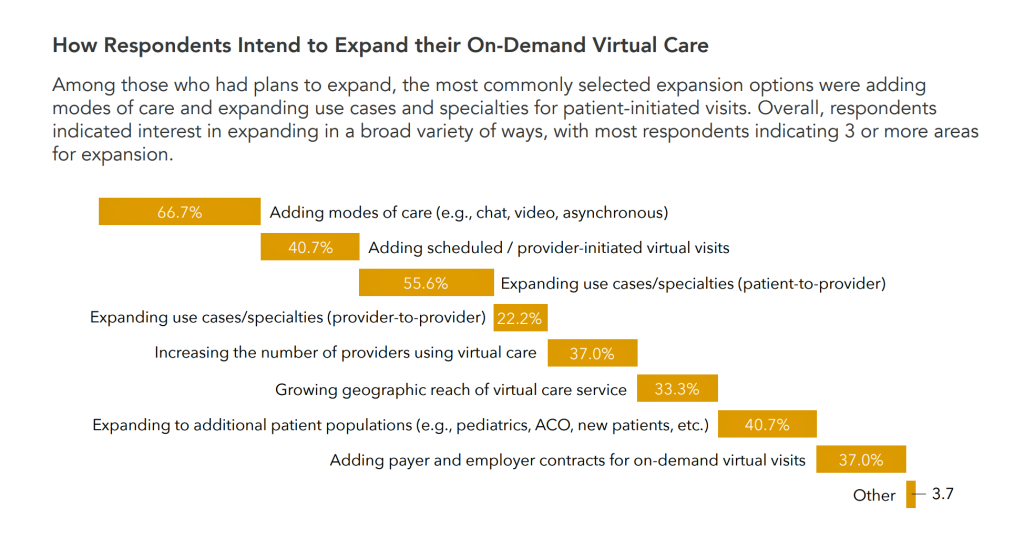

To reach patients where they live, work and play, most providers expanding telehealth plan to add different modes of care such as chat, video, and asynchronous communication between clinicians and consumers, shown in the horizontal bar chart. Over half will also add access to physician specialists. These program expansions are value-addes to the basic telehealth value proposition, allowing providers to tailor the telehealth program to a targeted patient population based on consumers’ values, medical conditions, and media/communications preferences.

Telehealth providers have varying program objectives: the top ranking goals are to remove patients’ geographic access to care, enhance patient experience through convenient care options, and to enhance market position to offer innovative care delivery. A fourth goal, for about one-third of providers, is to reduce the cost of care for risk-based population by siting care at lower-cost sites.

Telehealth providers have varying program objectives: the top ranking goals are to remove patients’ geographic access to care, enhance patient experience through convenient care options, and to enhance market position to offer innovative care delivery. A fourth goal, for about one-third of providers, is to reduce the cost of care for risk-based population by siting care at lower-cost sites.

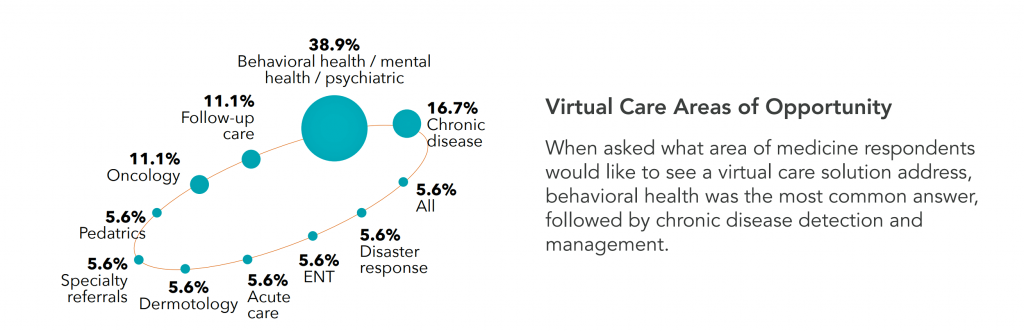

The “planets” chart illustrates health providers’ perceived areas of virtual care opportunity gleaned from the Zipnosis survey. Behavioral health and mental health features most prominently, sought by nearly 40% of providers. Addressing chronic disease was cited by 17% of providers, followed by follow-up care and oncology.

Health Populi’s Hot Points: My HIMSS19 panel on digital traction in consumerization in healthcare will focus on the case of telehealth featuring leaders from Walgreens, Cleveland Clinic, and Heal. Each of these organizations “do” telehealth in very different ways. We should consider telehealth through the consumer’s retail omnichannel lens, where patients-as-consumers-as-payors now look at health care as other life work-flows.

On that point, I’ll conclude with the story of Ro as in “Zero,” a consumer-facing health service designed to help smokers quit tobacco. The company built its own physician EMR, pharmacy software, and a pharmacy distribution center which already supports its first company, Roman (which deals with men’s health). Ro see’s itself as a “full stack” health care company, from diagnosis, prescription, treatment delivery all organized on one platform.

On that point, I’ll conclude with the story of Ro as in “Zero,” a consumer-facing health service designed to help smokers quit tobacco. The company built its own physician EMR, pharmacy software, and a pharmacy distribution center which already supports its first company, Roman (which deals with men’s health). Ro see’s itself as a “full stack” health care company, from diagnosis, prescription, treatment delivery all organized on one platform.

The company’s strategy is articulated on its website: “We promised to make the complicated straightforward. The expensive affordable. And the frustrating delightful.”

This is the goal of UX and service design in health care, long overdue in the industry. Zero and Roman are also part of telehealth. Ro will expand in women’s health in 2019.

The legacy health care system be forwarned: virtual health and telehealth are health care. Patients, as consumers and payors, are ready and waiting for you.

The post Telehealth and Virtual Care Are Melting Into “Just” Health Care at HIMSS19 appeared first on HealthPopuli.com.